In the United States, the top 1 percent of families owns more wealth than the bottom 95 percent of families combined. Millionaires own 80 percent of the country’s wealth while the bottom third of families owns none of it. Between 2007 and 2016, the average wealth of the top 1 percent increased by $4.9 million at the same time as the wealth of the median family declined by $42,000.1

Much has been written in recent years about the worsening of wealth inequality in America.2 This is an important story, but it can also mislead readers into thinking that midcentury America was an egalitarian society.

It was not.

In 1962, the bottom 40 percent of families owned just 0.3 percent of the national wealth while the top 1 percent of families owned 33 percent of the national wealth. Today, those figures are -0.5 percent and 40 percent respectively.3 Then, as now, the country was home to a large, propertyless underclass and high levels of overall inequality.

Wealth levels vary considerably by race, age, and education, but these intergroup differences are not why overall wealth inequality is so high. This can be demonstrated by looking at the distribution of wealth within each demographic group.

Percent of Wealth Owned by Top 10% of Demographic Group (2016)

In virtually every demographic group, wealth distribution takes on the same familiar pattern: the top 10 percent owns around three-fourths of the group’s wealth, while the bottom third owns none of it.

Why wealth in capitalist societies tends to concentrate like this has been a matter of much discussion over the years.4 Broadly speaking, it appears that capitalist economies contain feedback loops that cause relatively minor differences in initial endowments or incomes to become amplified over time. Those with more wealth receive more income; those with more income save at higher rates; and those who save at higher rates accumulate a larger share of the national wealth. In other words, wealth begets wealth.

In this paper, I propose that the US government tackle the problem of wealth inequality by creating a social wealth fund (swf) and issuing one share of ownership in the fund to every American. After the fund is created, the government will gradually accumulate assets for the fund to manage, such as stocks, bonds, and real estate. As the assets under management increase, the value of the shares held by the citizen-owners will increase, causing wealth inequality to fall. Although the citizen-owners will not be permitted to sell their shares, they will be paid a universal basic dividend (ubd) each year from the investment income earned by the fund.

Section One of the paper provides a basic background on social wealth funds. Section Two discusses the Alaska Permanent Fund, a social wealth fund created by the state of Alaska in 1976. Section Three contains a detailed proposal that federal policymakers could use to create an American social wealth fund along the lines explained above.

Our current policy discussion around wealth inequality is inadequate for the task at hand. This discussion features mostly small-bore proposals—often going under the heading of “low-income asset building”—that, if implemented, would have virtually no effect on the overall level of wealth inequality in the country. The goal of this paper is to go beyond these conventional proposals and provide a solution to wealth concentration that is designed to confront the monumental scale of the problem we face.

1

Background on Social Wealth Funds

Social wealth funds are generally defined as “collectively held financial funds, fully owned by the public and used for the benefit of society as a whole.”5 The concept is also sometimes referred to as “citizen’s wealth funds” or “sovereign wealth funds.”6 Whatever you call it, the idea is simple: the government directly owns a large pool of income-generating assets and then uses the return on those assets for social welfare purposes.

Interest in social wealth funds has spiked in recent years. Seth Ackerman proposed the creation of such a fund in 2012;7 Peter Barnes published a book on the subject in 2014;8 Tony Atkinson proposed the idea as a solution to inequality in his 2015 book;9 Angela Cummine and Stewart Lansley put out books about it in 2016;10 former Greek Finance Minister Yanis Varoufakis wrote in support of the idea in 2016;11 the pan-European movement DiEM25 included the idea in its European New Deal platform in 2017;12 and two British think tanks published reports promoting the idea in 2018.13 In addition to interest from policy writers, Hillary Clinton endorsed the concept of creating a national swf in her 2017 campaign memoir.14

The recent burst of writing on this topic was predated by a century of similar proposals. Rudolf Hilferding argued that the socialization of financial assets “constitutes the ultimate phase of the class struggle between bourgeoisie and proletariat” in 1910;15 Oskar Lange argued for the payment of a social dividend out of a collectively-owned capital stock in 1936;16 Nobel prize-winning economist James Meade published a paper in favor of the idea in 1964;17 and John Roemer proposed something similar to a social wealth fund in his 1994 book.18

The older swf advocates were typically motivated by market socialist ideologies. To them, a social wealth fund provided a way for society to collectively own, control, and benefit from the wealth of the nation. Although some modern swf advocates continue to argue for the idea on these traditional terms, most choose instead to present it as a practical and egalitarian source of revenue for social welfare purposes.

The turn towards the practical has likely been driven by the fact that the swf idea has now been successfully implemented many times throughout the world. At the beginning of 2016, the globe was home to around 80 sovereign funds spread across more than 60 governments, with most of the funds being established after the year 2000.19 Not all of these funds exist for a social purpose and so some do not meet the definition of a social wealth fund used above. But they all nonetheless prove that a government can own and manage large pools of income-generating assets without significant problems.

Sweden’sFailure

The most famous social wealth fund in history was the one briefly established in Sweden in the 1980s.20 The Swedish “wage-earner funds,” as they were called, were the brainchild of trade union economists Rudolf Meidner and Gösta Rehn. Meidner published a book on the idea in 1978 titled Employee Investment Funds: An Approach to Collective Capital Formation and then a retrospective paper in 1993 titled “Why Did the Swedish Model Fail?”21

Rudolf Meidner

The Meidner plan, as it came to be known, proposed using a scrip tax to gradually transfer ownership of Sweden’s corporations away from private shareholders and into wage-earner funds administered by the country’s labor unions. Under the plan, Swedish companies would be required to essentially pay a 20 percent tax on their profits. But rather than paying that tax in cash, they would instead issue an equivalent amount of new company stock to the relevant wage-earner fund.

Meidner calculated that, with an average profit margin of 15 percent and a continual reinvestment of profits back into buying more shares, the wage-earner funds would have majority ownership and thus control of Swedish companies after 25 years.

When Social Democratic Party (sdp) leader Olof Palme adopted the Meidner proposal ahead of the 1982 Swedish general election and then won, the whole world took notice.

The New York Times declared that it could be the end of the “middle way,” which they clarified as “the socialism carried on in Sweden from 1932 to 1976” that mostly left ownership in private hands. They went on to note the irony of the fact that the plan’s “transition to collective ownership” relied upon the country’s stock market, “the heart of capitalism.”22

The Christian Science Monitor called it a “Socialist program masterminded by Marxist economists of the Swedish Confederation of Trade Unions” and quoted various critics of the plan. Economist Per-Martin Meyerson is quoted as saying that, after the plan, “the market economy would cease to exist.” Stig Anderson, the manager of the Swedish band abba, is reported to have organized a concert “to help finance the fight against the Socialist takeover” and was quoted as saying an sdp electoral victory “might be the first time that a country will freely vote to go behind the Iron Curtain.”23

Despite the hysterical response, the plan was implemented in 1984, though in a diminished form. Under the program, the government imposed a relatively small excess-profits tax on companies rather than requiring them to directly issue new shares and created regional funds to hold the assets rather than the wage-earner funds originally proposed by Meidner. Nonetheless, the cash received from the excess-profit tax was used to purchase shares of Swedish corporations and the program managed to buy up 7 percent of Swedish company stock by 1991.

Unfortunately, after the country’s 1991 general election, Sweden formed a conservative government that put a halt to the program.

A lot of attention is paid to Sweden’s experience with the wage-earner funds. Leftist thinkers in particular often lament it as the last great push for practical, democratic socialism.24 But this mourning is mistaken. As noted already above, the world of social wealth funds is more vibrant now than it has ever been. In fact, over the past few decades, Norway, Sweden’s neighbor, has quietly put together the largest complex of swfs in the world, dwarfing what Sweden’s wage-earner funds managed to achieve.

Norway’sTriumph

Norway’s central government currently manages three main asset pools. There is the Government Pension Fund Norway (gpf-Norway), a stock and bond portfolio that is invested in Norwegian and other Nordic companies;25 the Government Pension Fund Global (gpf-Global), a stock, bond, and real estate portfolio invested exclusively outside of Norway;26 and the state-owned enterprises (soes), a set of 74 domestic companies that are directly owned by 12 government ministries.27

gpf-Norway and gpf-Global are social wealth funds. The soe assets, because they are owned directly by ministries rather than through a fund, are not technically a social wealth fund. But the soes are nonetheless in the spirit of a swf and could be rolled into a swf if the Norwegian state wanted to do so.

Adding up all of the wealth collectively owned through the Norwegian state produces some truly staggering figures. At the end of 2016, gpf-Norway controlled assets equal to 7 percent of Norway’s gdp;28 gpf-Global owned assets equal to 241 percent of gdp;29 and the soe equity holdings were valued at 23 percent of gdp.30 Thus, all together, the Norwegian central government owned assets equal to 271 percent of the country’s gdp in 2016. To put this in perspective, for the US government to own a similar amount of wealth, it would need to build a $54 trillion social wealth fund.31

The soes, gpf-Norway, and other local government funds combine to own a little more than one-third of all the equity listed on the Oslo stock exchange.32 This level of ownership is nearly 5× what the Meidner plan achieved before it was halted.

Folketrygdfondet Managing Director Olaug Svarva

Due to its collective wealth funds and soes, the Norwegian government owns around 59 percent of the country’s wealth. To reiterate: 6 out of every 10 kroner of wealth in Norway is owned by the state. When you exclude owner-occupied homes from the calculation, you find that the state of Norway owns 76 percent of the country’s non-home wealth. For comparison, the Chinese government owns only 31 percent of its national wealth.33

These holdings generate a considerable amount of income. Over the last 10 years, the conservatively-invested gpf-Global generated an average annual return of 5.9 percent.34 Over the same period, gpf-Norway had an 8.3 percent average return.35 In 2017, gpf-Global generated a return of 1,028 billion kroner while gpf-Norway had a return of 26 billion kroner.36 In 2016, the soe portfolio produced a 33 billion kroner dividend for the state.37 Adding the 2016 soe figure to the 2017 figures for gpf-Norway and gpf-Global gives you a total return of 1,087 billion kroner or $133 billion.38 Had that money been paid out as a dividend to all 5.2 million Norwegians, it would have provided each with $25,500, or $102,000 for every family of four.

The Norwegian funds are also efficiently administered. In 2017, gpf-Global’s expenses were equal to 0.06 percent of its assets under management and gpf-Norway’s expenses were 0.07 percent of its assets.39 These expense ratios are near the lowest in the world, even when comparing them to private asset management, and this is despite the fact that the funds are actively managed.

To be sure, Norway is an outlier in the world in terms of just how much wealth it has accumulated in its various swfs. But this is also what makes it such a promising example. The idea that a society could collectively own three-fourths of its non-home wealth through social wealth funds administered by a democratically-elected government without any negative economic consequences would be rejected as preposterous by most political and economic commentators in America today. But that is precisely what Norway has done and seemingly what any country could do if it has the necessary will and competence.

2

The Alaska Permanent Fund

The United States is already home to a handful of social wealth funds. There is the Permanent School Fund and Permanent University Fund in Texas,40 the State School Fund in Utah,41 and the Common School Fund in Oregon,42 to name a few. By far the most interesting and largest of those funds is the Alaska Permanent Fund (apf). What sets the apf apart from virtually all other swfs in the world is that the apf pays an annual cash dividend to every citizen of Alaska. It is thus a homegrown model of the kind of swf I think the federal government should implement on the national level.

The Alaska Permanent Fund (apf) only exists today because Alaska Governor Jay Hammond was obsessed with the idea of dividend-paying social wealth funds.43

Bristol Bay Failure

Before his stint as governor, during the 1960s, Hammond was the manager of a 2,000-person municipality in Alaska called Bristol Bay Borough. Bristol Bay was teeming with salmon resources, but 97 percent of those resources were being extracted by Seattle-based firms, not local fishermen. The Seattle-based firms even preferred hiring non-residents to staff their fishing operations, meaning that the local population was largely locked out of the job opportunities the salmon catch provided.

This situation resulted in serious economic deprivation for Bristol Bay residents: “no high schools, sewer or water systems, health care facilities, fire, police, or ambulance services.” The town’s garbage “was dumped over the riverbank in hopes it would flush out with the ice during high spring tides.”

Jay Hammond

Hammond hit upon an idea to reverse this dynamic. He proposed imposing a 3 percent tax on the fish catch and using the revenues to build out a “conservatively managed investment account” that would pay the residents an annual dividend from its investment returns. Since 97 percent of the fishing was done by non-local firms, this would mean 97 percent of the tax would be paid by non-local firms. Despite its seeming appeal, Hammond’s proposed ordinance failed at the polls, apparently due to anti-tax sentiments.

Hammond did manage to pass the tax a few years later in exchange for an elimination of the local property tax. The massive tax take from the fishing transformed the borough into the “richest municipality in the nation on a per capita basis” according to Fortune magazine, but Hammond nonetheless lamented his failure to establish a universal basic dividend in Bristol Bay.

Alaska Native Claim Settlement Act Failure

Undeterred by his mixed success at Bristol Bay, Hammond again tried to establish a dividend-paying social wealth fund in 1971 on the heels of a $900 million settlement that the federal government had entered into with the indigenous people of the state. Hammond was asked to make recommendations about how the natives could use that money and he suggested they put it in a big fund and use the investment return to pay annual dividends to all Alaskan natives.

As in Bristol Bay, Hammond’s idea was rejected. The native leadership decided instead to invest the money into the creation of over 200 native businesses. This was not the diversified social wealth fund of Hammond’s dreams, but the native-owned enterprises did nonetheless produce dividends for Alaskan natives in most cases.

SuccessAt Last

When Hammond became governor of Alaska in 1974, he found another opportunity to replicate what he did in Bristol Bay. The state’s gas severance tax was about half the national average, but most of the extracted gasoline was being sold abroad. So, he proposed doubling the gas severance tax, creating a $150 state income tax credit to offset any increase in gas prices in the state, and storing the remainder of the revenue in the general fund. This proposal passed.

Hammond’s tax-and-dividend proposal was a success, but not completely. “I found almost no one remembered the tax credit,” Hammond later wrote. “At that point I decided that if another dividend program were established, I wanted to put a check in everyone’s hand, rather than simply a credit for those making sufficient income to pay a state income tax. I thought that by so doing people would better recognize and appreciate the dividend concept and demand the state maximize returns from its resource wealth.”

And this is exactly what Hammond did. In 1976, he got the legislature to put a constitutional amendment on the ballot that would require that “twenty-five per cent of all mineral lease rentals, royalties, royalty sale proceeds, federal mineral revenue sharing payments and bonuses received by the State shall be placed in a permanent fund, the principal of which shall be used only for those income-producing investments specifically designated by law as eligible for permanent fund investments.” The measure passed by a 2-to-1 margin.44

In 1977, the Alaska Permanent Fund (apf) received its first deposit, $734,000 from oil royalties. In 1980, the legislature created a state-owned enterprise called the Alaska Permanent Fund Corporation (apfc) to manage the apf and created the Permanent Fund Dividend (pfd) program that began paying dividends to the citizens of Alaska two years later. Those dividends continue to flow to this day.45

After 15 years of trying, Jay Hammond’s dream of establishing a social wealth fund that paid out a universal basic dividend finally became a reality.

The Fund Today

At the end of 2017, the Alaska Permanent Fund owned just under $60 billion of assets.46 This is equal to around 113 percent of the state’s gdp.47 A similarly-sized fund for the United States would need to be around $22.6 trillion.

The assets are invested in a broad and diversified portfolio of stocks, bonds, real estate, and other ventures.

FY2017 Target Asset Allocation

Across its 34-year existence, the apf has achieved an average annual investment return of 8.78 percent. The apf’s performance is slightly below its benchmark index across the entire 34-year horizon, but quite a bit above that same index in more recent years. This seems to indicate that the apfc is getting better at asset management over time. Nonetheless, the main drivers of the apf’s return in any given year are general economic conditions.

Fund’s Long-Term Investment Performance

When the fund is operating normally, a portion of its investment return is plowed back into the fund for inflation-proofing purposes. The remainder of the return is transferred to the Alaska Department of Revenue in order to pay out the Permanent Fund Dividend (pfd) to citizens of the state. The dividend amount is calculated as “21 percent of the net income of the fund for the last five fiscal years.”48 This calculation essentially means that the dividends are based on a 5-year moving average of the fund’s return. Both the inflation-proofing and dividend issuance is subject to the legislature’s approval, which it has occasionally withheld.

In 2017, Alaska’s government paid out a dividend of $1,100 to 629,859 citizens. This is equal to $4,400 for a family of four. In an unusual move, the $1,100 dividend was dictated by a legislative action, as opposed to the statutory formula, and was lower than it would have been under the formula.49 In prior years, the dividend went as high as $2,072, or $8,288 for a family of four.

ProgramEffects

Despite its novelty and size, there have been relatively few serious efforts to evaluate the apf’s effects. One reason for this might be that “many people view the pfd as a distribution of income from assets owned by individual citizens rather than as an appropriation of government.”50 Put differently: because Alaskans generally view their dividend income as coming from their ownership of the fund, they seem to think that how people spend it, and other similar questions, are irrelevant.

Nonetheless, we do know that, all else equal, a flat dividend payment like this should reduce inequality in the state. Receiving $8,000 in dividend payments increases the income of a family with $20,000 of earnings by 40 percent and the income of a family with $200,000 of earnings by 4 percent. This sort of pattern will compress the distribution of the state’s disposable income under typical inequality measures and, in 2016, Alaska was the most equal state in the country.51

Similarly, we know that a payment like this should reduce poverty in the state. Figuring out just how much it reduces poverty is difficult because Census income surveys frequently fail to record dividend income for Alaskans. But one estimate from Matthew Berman and Random Reamey suggests that the payment reduces the poverty rate in the state by 20 percent.52

Some might worry that these sorts of dividend payments could significantly reduce employment in the state because they make working less necessary for survival. But a study by Damon Jones and Ioana Marinescu found that the dividend had no effect on overall employment rates, though it did seem to coincide with higher levels of part-time, as opposed to full-time, work.53 Jones and Marinescu also found support for the theory that the dividend payments increase consumption and thereby increase demand for labor in the state.

Although the precise economic effects of the program are somewhat unclear, public opinion about the program is not: the Alaskan people love it.54

Forty percent of Alaskans say the dividends make a “great deal or quite a bit of difference in their lives.” Thirty-nine percent say they make a “fair amount or only some difference” in their lives. Only 20 percent say they make no difference. Those saying the dividends make the most difference in their lives are women without a college degree, unmarried women, mothers with children, and native Alaskan women.

Nearly 80 percent of Alaskans say “the pfd checks are an important source of income for people in my community.” Eighty-four percent agree with the statement “as owners of the Alaska Permanent Fund, Alaska residents are entitled to an equal share of the earnings of the fund,” and 74 percent take that all the way to its extreme, saying they agree that millionaires should receive the dividend as well.

The apf is so beloved in Alaska that 64 percent of residents would rather create a state income tax (Alaska currently lacks one) rather than reduce dividends in order to cover the state’s projected budget shortfall. To reiterate: residents in one of the most conservative states in the country support paying a state income tax in order to preserve a universal basic dividend program.

3

The American Solidarity Fund

The United States government should create a national social wealth fund along the same lines as the Alaska Permanent Fund (apf). For the purposes of this paper, I will call this proposed fund the American Solidarity Fund (asf).

ASF logo permutations

The American Solidarity Fund will operate the same way that any other social wealth fund operates. Money and assets will be placed into the fund; a public entity will manage those assets in a way that generates investment returns; then those investment returns will be used to fund social spending, in this case a universal basic dividend for the citizens of the country.

The remainder of this section provides details for the various aspects of the asf. Not every detail is essential and there are multiple ways to do most things. Where multiple options exist, I try to detail all of the options and provide my recommendation.

Bringing Assets into the Fund

Generally speaking, there are five ways to bring assets into a social wealth fund: voluntary contributions, ring-fencing existing state assets, levies, leveraged purchases, and monetary seigniorage. I recommend all of the above, but think only the latter three are likely to provide substantial ongoing inflows of assets.

Voluntary Contributions

Adding assets to the asf through voluntary contributions is pretty simple. The administrators of the asf will create a way for people to donate money or other kinds of assets to the fund and the government will encourage people to contribute.

Lynn Stout and Sergio Gramitto favor this approach in their social wealth fund proposal.55 In their paper, they argue that “ultra-high-net worth individuals are a significant potential source of [social wealth fund] donations” in part because “this cohort already frequently participates in philanthropy” and because, for the ultra-wealthy, “philanthropy is the only real place money can go.” They also note that “if the top decile of equity holders contribute half their holdings to [the social wealth fund], while living or upon death, the fund would within a few decades come to hold forty percent of all corporate equities.”

Stout and Gramitto argue that corporations might “also have reason to donate their own shares.” Contributions to the fund would be good public relations and could be used by companies to counterbalance “the influence of short-term shareholders, especially activist hedge funds.”

I am skeptical that the level of voluntary contributions would be high enough to create an adequately-sized social wealth fund. But certainly nothing is lost by allowing such contributions to be made.

Ring-Fencing Existing Assets

Another way to grow the fund would be to transfer existing state assets into it. Dag Detter and Stefan Fölster are the most prominent advocates of this approach.56

The United States government owns a large amount of physical assets. Those assets include over 450 million acres of land valued at $1.8 trillion,57 over 900,000 buildings worth hundreds of billions of dollars,58 thousands of miles of intercoastal waterway, and countless infrastructure projects. The government also owns the electromagnetic spectrum, which it currently auctions off to telecommunications companies.

After depositing these and other existing assets into the asf, the fund could generate investment income from them by renting them out or, where appropriate, selling them and using the revenues from the sales to buy other more promising assets, such as stocks and bonds. Some of the land and building assets are already being used by the federal government for other purposes. After making the asf the owner of the land and buildings, the other governmental agencies could be made to pay rent to the asf for their use.

Insofar as handling physical assets is labor intensive, this particular source of assets will probably be the most difficult to manage.

Levies

The government could also bring assets into the fund through levies, i.e. taxes and fees.

Any type of levy could conceivably serve this purpose. For instance, Peter Barnes proposed, among other things, a value-added tax on the telecommunications sector, which is a type of consumption tax.59 During its 1971 Congress, Denmark’s trade unions proposed building a social wealth fund using a payroll tax, which is a type of labor tax.60

Although levies on consumption and labor can work, levies on capital seem to be a more natural way to go. After all, the purpose of a social wealth fund is to transfer wealth into a collective pool. Applying new levies directly on wealth seems to serve that purpose the best. Thus, what follows are a variety of capital taxes and fees that I think would be ideal mechanisms for bringing assets into the asf.

One-time market capitalization tax.

To jump start the fund, the government could impose a one-time tax on the market capitalization of public (and possibly non-public) companies. Companies would have the option of paying this tax in cash or through scrip, i.e. by issuing new shares to the asf. The sec already imposes a 0.01245 percent market capitalization tax on newly-issued securities, which it calls a “filing fee.”61 At the end of 2017, the market capitalization of listed domestic companies was $32.1 trillion.62 A one-off 3 percent market capitalization tax would thus bring in around $1 trillion of assets. And this would amount to only a few months of the total return provided by the stock of these companies.

Ongoing market capitalization tax.

To continue bringing money into the fund, the government could impose ongoing market capitalization taxes. This would be done at a lower rate, e.g. 0.5 percent per year. As with the one-time tax, the sec could administer this ongoing tax since it already imposes such a tax on newly-issued securities.

IPO tax.

When a company goes public through an initial public offering (ipo), its stock becomes much easier to trade. This “liquidity” is highly valued by investors and so they are willing to pay more money for publicly-traded stock than they are for private equity. This “liquidity premium” is estimated to increase the value of publicly-traded stock by around 20 to 30 percent.63 Since it is the government that creates the uniform and tightly-regulated securities markets that make this liquidity premium possible, it stands to reason that it should share in the value it creates. The 0.01245 percent market capitalization “filing fee” currently charged by the sec is too low. It should be raised to, for example, 5 percent (payable in scrip or cash). For consistency purposes, the ipo tax should also be assessed when public companies acquire private companies.

Mergers and acquisitions tax.

The government could impose a tax (payable in scrip or cash) on companies that merge with or acquire other companies. The ftc already imposes such a tax in the form of the fees it collects during premerger reporting under the Hart-Scott-Rodino (hsr) Antitrust Improvements Act of 1976.64 The current hsr fees range from $45,000 to $280,000 depending on the value of the transaction in question. The new tax should be much higher, e.g. 3 percent of the value of the transaction with some minimum threshold so as to exclude very small businesses. The ftc can collect the tax just as it already collects the hsr fees. To avoid duplication, this tax would only be assessed where the ipo tax discussed above is not assessed.

Financial transactions tax.

The government could levy modest taxes on the volume of financial transactions. Dean Baker estimated in 2016 that a 0.2 percent tax on stock trades, a 0.1 percent tax on bond trades, and a 0.002 percent tax on derivative trades would bring in around $120 billion, or 0.6 percent of gdp.65 It is worth noting that the sec already has a very modest financial transactions tax. It is set at 0.00231 percent of the value of securities transactions.66 Finra also charges a Trading Activity Fee (taf) for certain securities transactions, which is similar to a financial transactions tax.67

Securities custodian tax.

Most securities are held by a custodian company such as the Depository Trust Company (dtc). When securities are traded, they do not change hands, but rather book-entry changes are made by the custodian indicating the new owner. The dtc boasts that it is the custodian of “more than 1.3 million active securities issues valued at us$54.2 trillion as of 7/31/2017.”68 An annual tax on securities custodians of 0.1 percent could pull in $54 billion from the dtc alone. Presumably the dtc would pass that along to the companies issuing the securities.

Fund management tax.

Many investors own shares of funds that themselves own large baskets of various securities. These funds make money by charging fees equal to a percentage of the assets in the funds. Typical management fees are between 0.51 percent of assets and 0.74 percent of assets depending on the fund type.69 Some go as low as 0.03 percent.70 The federal government could impose its own assets under management (aum) tax for these kinds of funds, e.g. 0.05 percent. Fund managers would pass this through as slightly higher management fees for their overwhelmingly affluent investors.

Inheritance and gift tax.

The US only has a tiny tax on very large estates despite the fact that around 60 percent of US wealth has been inherited.71 Inheritance and gift taxes should be massively increased with their revenues going into the asf as a collective inheritance for everyone, not just the children of the affluent.

Elimination of certain tax expenditures.

The US currently has a variety of tax breaks oriented towards promoting individual asset-building. These tax breaks are giveaways to the rich and do not even appear to achieve their stated purpose of incentivizing saving.72 These tax expenditures should be eliminated and the revenue redirected to the asf, which will directly increase the wealth of everyone in the country by an equal amount. The Joint Committee on Taxation recently estimated that, in 2018, the mortgage interest tax deduction and the exclusion of capital gains on sales of principal residences cost $105 billion; the reduced tax rates on dividends and long-term capital gains cost $135 billion; the exclusion of capital gains at death cost $35 billion; and tax exclusions for pension and ira contributions cost $240 billion.73 All together, that’s $515 billion per year.

These are not the only possible levies, but they are particularly promising levies that directly embody the idea of shifting assets away from the wealthy and into a collective fund.

Leveraged Purchases

The government could also borrow money at low interest rates to invest in financial assets with high rates of return. Between 1990 and 2017, the average interest rate for a 1-year treasury bond purchased on the first day of the year was 3.17 percent.74 During the same time, the average total return of the s&p 500 was 11.3 percent.75 The difference between them, 8.13 percent, is the approximate rate of return that could be accomplished by an asf that issued government debt in order to buy stock equity.

For example, if the asf had existed between 1990 and 2017 and borrowed $1 trillion per year at the prevailing 1-year treasury bond rate and invested that $1 trillion into the s&p 500, it would have generated a cumulative return over the period of $2.275 trillion (nominal dollars). That return could have been directly parceled out as dividends or been deposited towards the principal of the asf.

In the above example, the asf issues debt and buys stock regardless of the relative price of each security. In a more realistic scenario, the asf would be able to make better decisions about when such a move is the most likely to generate an investment return. So, it would not borrow money to invest when treasury rates or price-to-earnings ratios are especially high.

In general, because the return on us government debt is lower than the return on other kinds of marketable securities, the us government should be able to take advantage of that spread to generate investment returns.

Monetary Seigniorage

The Federal Reserve makes adjustments to the money supply by purchasing securities through open market operations. The way this works is that the Federal Reserve creates new money and then buys assets with it. Right now, the Federal Reserve almost always chooses to buy Treasury bonds. But the government could require that the Federal Reserve inject money into the system by buying more lucrative securities such as publicly-traded equities.

This is what the Bank of Japan (boj) has been doing for the last few years. In January of 2008, the boj owned just 1.5 trillion yen of stocks, shares of exchange-traded funds, and shares of real estate investment trusts.76 In May of this year, the same figure was 21.1 trillion yen, which is equal to $193 billion.77

During the same period, the Federal Reserve also expanded its balance sheet considerably by buying Treasury bonds. In January of 2008, the Federal Reserve owned $740 billion of Treasury bonds. In May of this year, it was a little under $2.4 trillion.78 Had the Federal Reserve instead chosen to buy up total stock market exchange-traded funds, like the Bank of Japan did, it could have profited handsomely off of the massive stock market rise over that period. And if those assets were connected to the asf, the profits could have been paid out to everyone in the country through the corresponding universal basic dividend program.

In addition to directing the Federal Reserve to buy other kinds of securities, the government could also adopt a higher inflation target (e.g. 4 percent rather than the current 2 percent), an idea that already has significant support on the merits.79 A higher inflation target would permit larger expansions of the money supply and therefore enable more purchases of return-generating assets.

Managing the Fund

After assets are brought into the asf, they have to be managed in some way. The management of asf presents three main questions: 1 what entity will manage it, 2 what assets will it hold, and 3 how will it exercise its ownership rights over its assets? These questions are answered in order below.

1 The Managing Entity

The cleanest way to manage the asf is by creating a new state-owned enterprise (soe) that is fully owned by the Treasury Department and then “hiring” that soe to be the fund manager. This is the model used by the Alaska Permanent Fund and gpf-Norway. In Alaska, the soe is called the Alaska Permanent Fund Corporation and in Norway it is called the Folketrygdfondet.80

Folketrygdfondet Management Team

The way this would work in practice is that, pursuant to an act of Congress, the Treasury Department would create a new corporation. Let’s call it the American Solidarity Fund Corporation (asfc). The Treasury would formulate articles of incorporation for the asfc and appoint its board members, board chairs, and auditor. From there, the asfc’s board would be responsible for the management of the asfc, including the election of the asfc’s ceo.

Once the responsibility for managing the asf is handed over to the asfc, the Treasury would not be involved in the day-to-day operations of the fund. But it would be able to create rules, mandates, directives, and other sorts of guidance that the asfc would have to follow. This kind of separation will reduce the administrative burden that the Treasury has to take on itself and provide a certain level of operational independence for the fund managers.

As with the Alaska Permanent Fund Corporation, we should expect the asfc to start out as a fledgling organization and evolve over time into a mature and professionalized operation. This evolution would also likely mean that the asfc would initially rely on some level of outsourcing to carry out its business, but, in the medium and long term, would seek to do all of its fund management with its own staff.

2 Asset Allocation

What assets the asf will hold is ultimately a political question that will, in practice, be answered by the us Congress or by Treasury mandates that the asfc has to follow. swfs across the world have taken all sorts of approaches to asset allocation and so it is difficult to say there is any settled approach.

One possible approach to asset allocation would be to initially invest in easy-to-manage listed securities like domestic and international equities and bonds. As the fund gets bigger and the asfc becomes a more mature organization, it may make sense to broaden the asf portfolio to include unlisted assets like private equity and real estate.

When thinking about asset allocation, it will be important for decision-makers to consider how best to leverage the unique attributes of the asf: its size, long-term horizon, and low need for liquidity.

In addition to making general asset allocation decisions, the asf could also make narrow allocation decisions that pertain to specific companies. For instance, the Treasury or us Congress could create a process for excluding companies from the fund if those companies are found to violate established guidelines, such as engaging in human rights violations or environmental destruction. Norway’s gpf-Global maintains an exclusion list along these lines.81

3 Ownership Rights

Since the asf will own shares of companies, it will have the ability to exercise the ownership rights that those shares confer, i.e. vote on shareholder matters like the election of the board and shareholder resolutions. There are three basic approaches to exercising ownership rights:

No Voting. The first approach is to abstain from voting, i.e. to opt out of exercising ownership rights. This is the approach favored by Dean Baker.82 In this scenario, only the remaining private shareholders would vote on board members and shareholder resolutions.

Representative Voting (recommended). The second approach is to make voting decisions through the country’s government. What this means in practice is that the Treasury would issue voting guidelines that the asfc would have to implement on a vote-by-vote basis. For instance, the Treasury could create ceo pay guidelines that the asfc must follow when casting shareholder votes for or against ceo pay packages.

Direct or Proxy Voting. The last approach is to allow the citizen-owners to directly vote on shareholder matters through a website maintained by the asfc. This is the method favored by Lynn Stout and Sergio Gramitto.83 Under this approach, citizen-owners would be allowed to either vote directly on shareholder questions or give away their voting rights to a proxy organization that they trust to exercise them in their interest. Proxy organizations would register with the asfc so that they could be selected on the website and citizen-owners would be permitted to change their preferred proxy organization at any time. For instance, a citizen-owner who was interested in labor rights might give their votes to the afl-cio while a citizen-owner who was interested in the environment might give their votes to the Sierra Club.

In my view, the no-voting option is a serious mistake. If the government does not vote its shares, then it is ceding total control of corporations to the most affluent people in society. It is fair to worry that the government might make bad shareholder votes from time to time, but not reasonable to think that very affluent people will on average make better shareholder votes than a democratically-elected government.

Between the other two options, I have a slight preference for representative voting, at least initially. In the early years, the asf and asfc will need to focus their organizational time on more important implementation challenges and will not own enough assets for their shareholder votes to make much of a difference anyways. Over time, it could make sense to add a direct or proxy voting system.

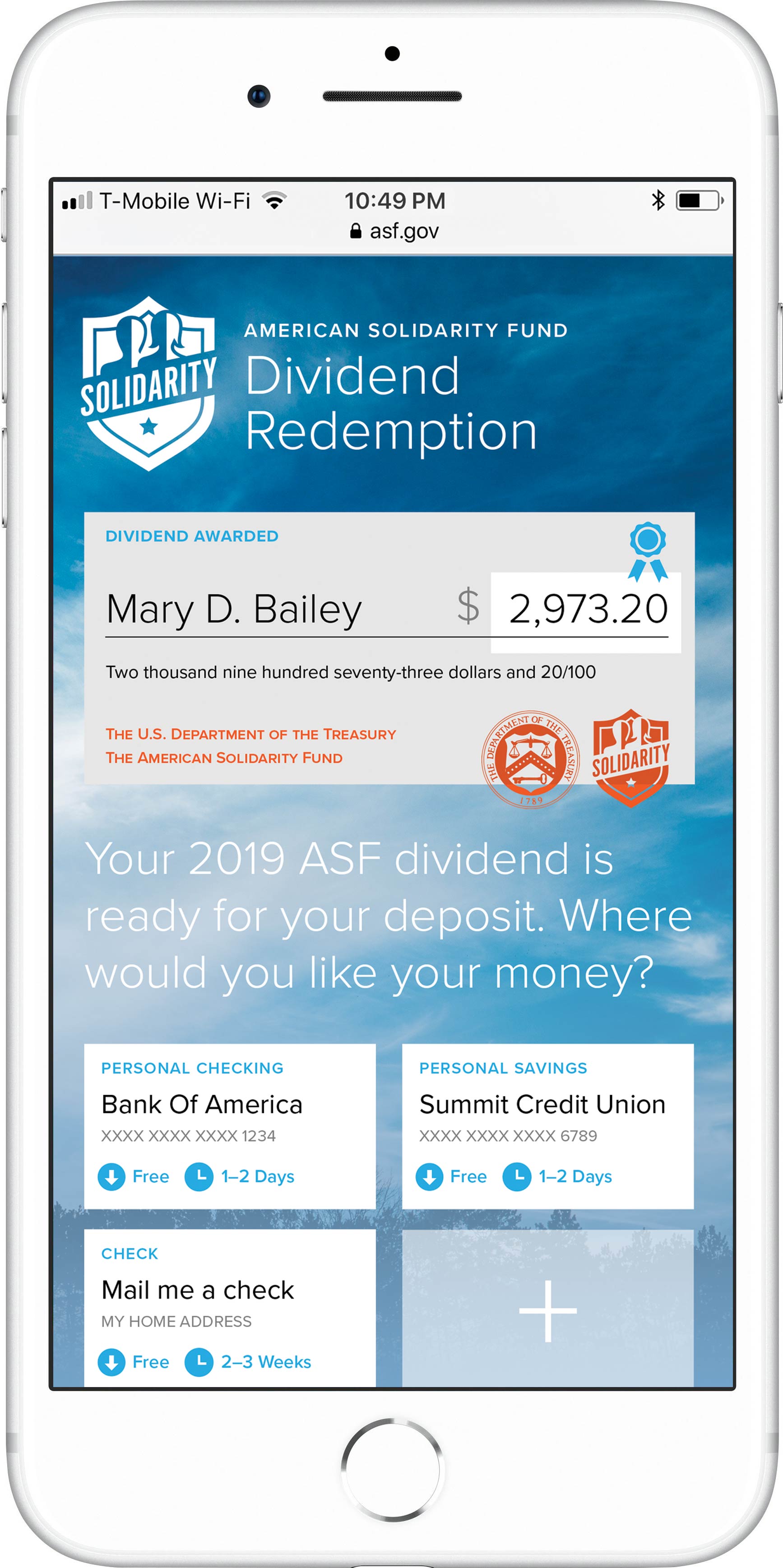

Universal Basic Dividend

The final aspect of the asf is the easiest one: paying out the universal basic dividend (ubd) from the return on the fund. Alaska already provides a concrete model for how to do this, but I would recommend some cosmetic and substantive modifications to the Alaskan approach.

ASF Ownership Shares

Every qualifying citizen should be given one nontransferable share of ownership in the asf, which is what entitles them to receipt of the ubd. The Alaska Permanent Fund does not provide any kind of formal ownership shares, but the residents of the state nonetheless conceptualize themselves as joint owners of the fund. The idea of providing a quasi-formal ownership share was supported by the 1971 Danish trade union proposal, which would have provided each owner “an annual certificate setting out their entitlement in the fund” that “could not be sold for at least seven years” and even then could only be sold “back to the fund itself.”84 Unlike the Danish proposal, I am recommending that the citizen-owners never be permitted to sell their ownership share and that the share remit back to the asf upon its owner’s death.

As part of this ownership arrangement, the asfc should have a website that looks like the sites run by Vanguard or Fidelity where citizen-owners can log on and see their single share of ownership, track its value over time, and so on. This is also where they would input their banking information and address to receive their dividend checks. The purpose of the website and the ownership share generally is to impress upon people that this is their collective wealth fund. This is partially a communications gimmick, but no more so than many of the hyper-abstracted ownership gimmicks that already exist in the country’s capital markets.

Dividend Amount

The dividend amount should be set equal to a five-year moving average of a percentage of the asf’s market value. The percentage would be set legislatively or by the Treasury and would aim to, on average, withdraw an amount equal to the inflation-adjusted return of the fund. This is a hybrid of the way Norway’s gpf-Global and the Alaska Permanent Fund currently manage fund withdrawals.

So, for example, the rule could be that 4 percent of the five-year moving average of the asf’s market value will be withdrawn each year and used for the ubd. If the asf’s value over the last five years was $8 trillion, $9 trillion, $10 trillion, $11 trillion, and $12 trillion, then the dividend withdrawal would be 4 percent of $10 trillion, or $400 billion.

Using a specific percentage of market value makes withdrawals administratively easy and using a five-year moving average of market values smooths out market volatility in asset prices, ensuring that the dividend amounts do not swing wildly year to year.

Dividend Eligibility

Alaska provides its dividend to every citizen of the state, including children. I would recommend excluding children from the asf dividend. Under this proposal, every citizen over the age of 17 would receive an ownership share and thus a dividend. Families with children should receive child allowances for each of the children they are caring for, but that should be done through a different program.

In an ideal construction, retired people would also be ineligible for a dividend. As with children, retired people are owed a cash income, but they already receive such an income through Social Security’s old-age pension. Excluding children and the retired from ownership and dividends would allow the dividends to be higher by reducing the number of beneficiaries.

In practice, excluding the retired seems like it would be difficult to do. The retired are a large voting bloc and many of them are dependent on private capital ownership for their retirement income. Since the asf proposal intends to shift some of that capital ownership into a collective fund, they will need to be included in the asf’s ownership as well.

Conclusion

At the end of 2017, households and nonprofit organizations had a collective net worth of $98.7 trillion.85 By now, it is above $100 trillion. But this wealth, and the income it generates, is overwhelmingly owned by a small class of people at the top of society. If we want to get serious about reducing wealth and income inequality, then we have to get serious about breaking up this extreme concentration of wealth.

A dividend-paying social wealth fund provides a natural solution to this problem. It reduces wealth inequality by moving wealth out of the hands of the rich who currently own it and into a collective fund that everyone in the country owns an equal part of. It then reduces income inequality by redirecting capital income away from the affluent and parceling it out as a universal basic dividend that goes out to everyone in society.

Social wealth funds have a long track record of success throughout the world, including in our own country on the state level. It is not a pie-in-the-sky idea, but rather a practical plan with dozens of working models currently in operation. There is an alternative to crushing inequality. The only question is whether we will choose it.

Image taken from “Travels into Poland, Russia, Sweden, and Denmark. Interspersed with historical relations and political inquiries. Illustrated with charts and engravings.” (The British Library)

Fisherman (U.S. National Archives: Department of the Interior. National Park Service. Alaska Region.)

Pat Le Donne on eastern Twin Lake (U.S. National Archives: Department of the Interior. National Park Service. Alaska Region.)

Jay Hammond (Alaska Blue Book [Second edition], Alaska Department of Education, Division of State Libraries)

Eskimo family on spring ice of Krusenstern Lagoon on an egg hunting trip (U.S. National Archives: Department of the Interior. National Park Service. Alaska Region.)

Artist On Bank Of The Schuykill River (U.S. National Archives: Still Picture Records Section)

Folketrygdfondet management team (Folketrygdfondet Annual Report 2017) Postcard—Norway: Danebu, Aurdal. Valdres (National Library of Norway)

Postcard—Norway: Party from the road Røldal - Sauda. In the background Røldal. (National Library of Norway)