For most of the twentieth century the stock market made only small gains compared to the golden era we are living in today. Since the 2008 financial crisis, markets have soared and, month after month, the major stock indexes have broken new records. In July, the NASDAQ and the S&P 500 broke new all-time highs, with the Dow Jones not far behind. The stock market has not just recovered from the financial crisis. It is making serious bank.

One of the stock market’s most popular cheerleaders has been President Donald Trump. Since July, Trump has sent out eleven tweets championing the strength of the stock market. Two in particular seem to suggest that a rising stock market goes hand in hand with increased wages:

Stock Market at all time high, unemployment at lowest level in years (wages will start going up) and our base has never been stronger!

— Donald J. Trump (@realDonaldTrump) July 2, 2017

Highest Stock Market EVER, best economic numbers in years, unemployment lowest in 17 years, wages raising, border secure, S.C.: No WH chaos!

— Donald J. Trump (@realDonaldTrump) July 31, 2017

Former President Barack Obama was a bit more discerning when he compared the stock market to wages. However, he still used the stock market as a yardstick to measure the strength of the economy. A few years after the financial crisis, when the stock market began to pick up, Obama said in his 2011 State of the Union Address:

Two years after the worst recession most of us have ever known, the stock market has come roaring back. Corporate profits are up. The economy is growing again.

Our political leaders seem to suggest a soaring stock market means great things for our country. But, what does the stock market do for average Americans? More specifically, what does it do for their wages?

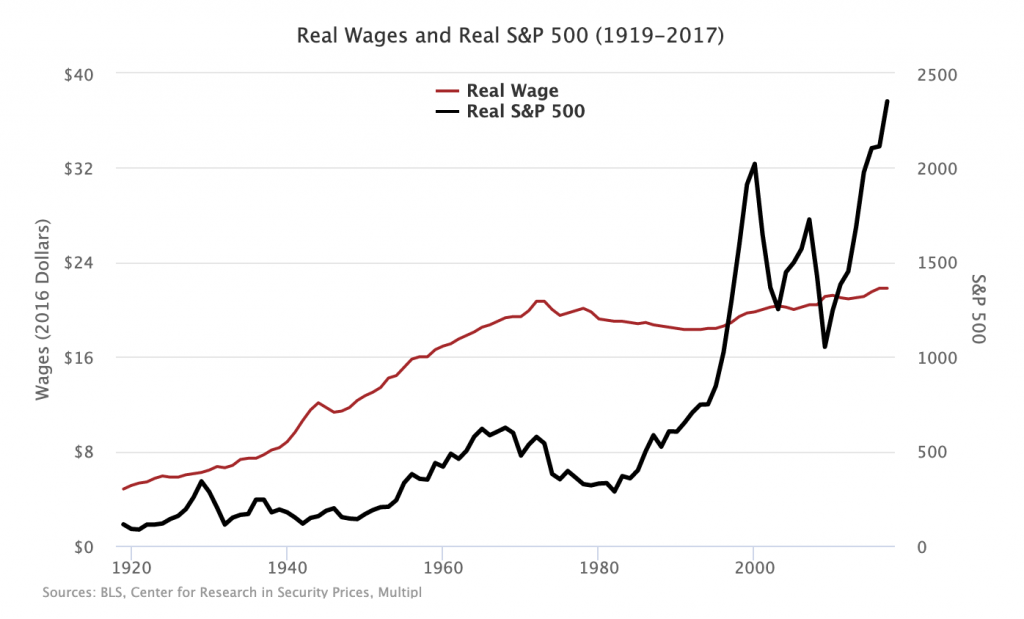

The figure above compares the average real wages of nonsupervisory workers and the real level of the S&P 500 from the early twentieth century to today. Both series are adjusted for inflation using the CPI (pre-1978) and CPI-U-RS (post-1978).

To begin, let’s look at real wages measured in 2016 dollars. From 1920 to the early 1970s, real wages rise quickly and consistently. But in the mid-1970s real wages begin to decline. Then in the mid-1990s wages begin to slowly rise. The S&P, on the other hand, behaves quite differently. From the 1920s to the early 1970s it also moves upward, but slowly. Then the S&P rapidly shoots up just as wages begin to decline.

Let us study the figure in more detail. Before 1980, real wages grow at an average rate of two and one half cents ($0.025) per month. Then, after 1980 wages grow by only an average rate of 0.7 cents ($0.007) per month – a 71 percent drop in the average rate of growth. The S&P 500 follows a different pattern. Before 1980, the S&P grew at an average pace of 0.53 points per month. But, after 1980 the S&P begins to soar. The index increases by 4.0 points per month – a 660 percent rise in its growth rate.

Looking at this more abstractly, how does the real wage respond when the S&P increases by one point? Before 1980, when the S&P rises by one point, on average the real wage increases by three cents ($0.027). After 1980, when the S&P rises by one point, the real wage increases by only one tenth of one cent ($0.001).

This leads us to ask: Are these two variables even correlated? When the S&P increases, does the real wage also increase? Correspondingly, when the S&P decreases, does the real wage decrease? From 1950 to 1975, they were largely positively correlated. But after 1975, the correlation tended to be more negative than positive. Meaning, when the S&P increases the real wage tends to decrease, and when the S&P decreases the real wage tends to increase. After 1975, on average, while one was moving up the other was moving down.

Political leaders seem to believe that what’s good for the stock market is good for the larger economy. But the data show that since the 1980s, when the stock market rises, wages barely move. Today, hourly wage earners – who constitute nearly 60 percent of the workforce – are only making slightly more on average than they did forty years ago. In fact, if the federal minimum wage kept pace with the average hourly wage and average productivity since the late 1960s, it would be over $18 per hour today.

Yet, political and business leaders still proceed as if the stock market is key to measuring the success of the economy. Perhaps the stock market tells us about the prospects of capital owners, but it certainly doesn’t tell us much about the average worker.