If Republicans win the House or the Senate in the coming midterms, they may use the debt ceiling to try to negotiate cuts to the Social Security program. As noted last week, these cuts are generally described as increases to the retirement age, but they don't actually change at what age people can retire. They just cut benefit levels at all 96 Social Security retirement ages.

Underlying most efforts to cut Social Security benefits is the claim that Social Security is facing "insolvency." This is a scary word that is neither technically accurate nor effective at getting people to understand the thing the word is used to describe.

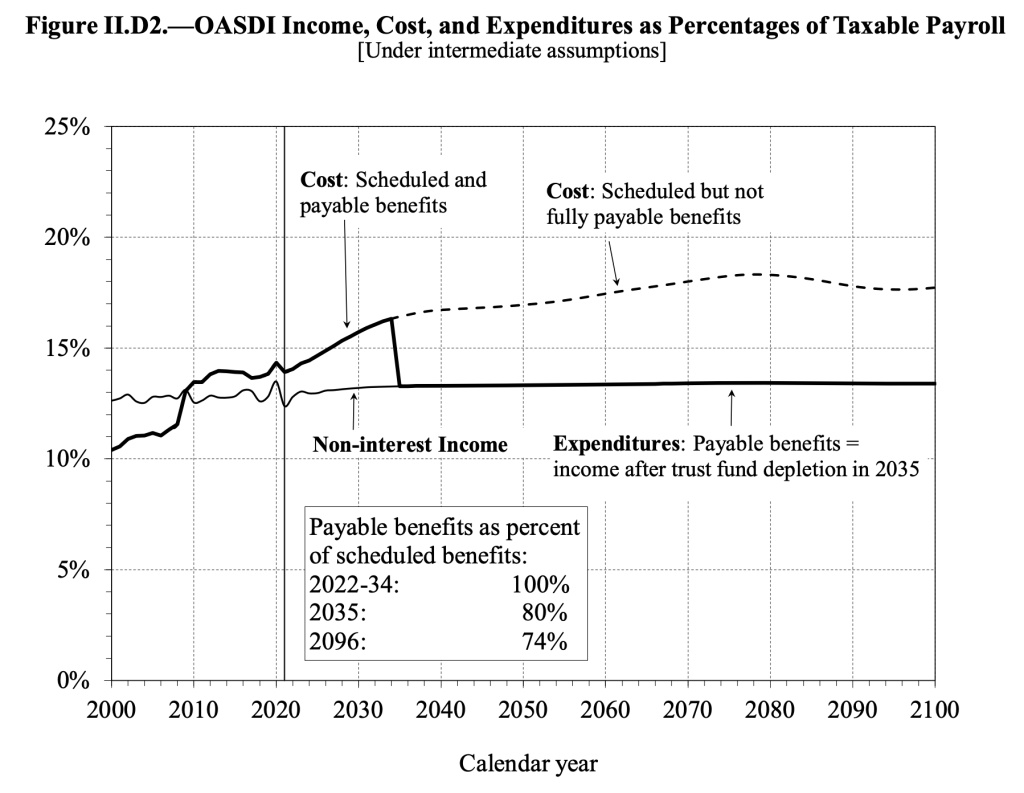

Under current law, Social Security cannot technically become insolvent because the program's benefit levels are constrained by a solvency requirement. When the aggregate amount of benefits people could receive under the Social Security formula exceeds the revenues and trust fund assets, this triggers an across-the-board benefit cut to make sure that the two sums are balanced.

According to the latest Social Security projections, absent program changes, this benefit cut will be triggered in 2035 and will amount to a 20 percent reduction in 2035, growing to a 26 percent reduction in 2096.

This differs from what people generally think of when they hear the word "insolvency," which is that the program will collapse entirely and benefits will stop going out. That is not what will happen.

In fact, the thing advocates call "insolvency" — an across-the-board benefit cut — is really no different than raising the retirement age. In the scenario graphed above, "insolvency" results in a 20 percent reduction in benefits in 2035. By contrast, "raising the retirement age to 70" is a 23 percent benefit reduction. So "raising the retirement age" doesn't avoid "insolvency" as these are just two opaque phrases used to describe the exact same policy.

The main reason advocates are able to frighten people with the specter of insolvency is because of the current law that requires the Social Security program to respond to revenue shortfalls by cutting benefits. But policymakers could easily change this trigger and they should.

For example, the relevant law could be amended to state that, whenever revenue falls short of scheduled benefits, the Social Security payroll tax will automatically be increased to make the two sums balance. In fact, you could get even cuter with it and make it so that revenue shortfalls trigger Social Security payroll tax increases only on earnings exceeding $150,000 or similar.

Changing the trigger in this way would not require any new taxes or really change anything at all about how the program operates in the near term. All it would do is change the default outcome of so-called "insolvency." No longer would "insolvency" mean automatic benefit cuts. It would instead mean automatic tax increases on the rich. This change would hugely alter negotiations over the Social Security program while completely undercutting the ability of austerity-minded organizations and commentators to mislead and terrify people about Social Security's future as part of their agenda to cut the program.