The Norwegian Government recently released its tax proposal for 2023 in English. The document contains many insights that could be applied to the US as well as a corrective to certain US discourses about Nordic taxation.

1. Vehicle Taxes

When a Norwegian purchases and registers a new vehicle, they are assessed three main taxes: a weight tax, a carbon (CO2) emissions tax, and a nitrogen oxides (NOx) emissions tax.

In the tax proposal, the NOx tax is set equal to $12.67 multiplied by the number of milligrams of NOx that the vehicle emits per mile driven. The Bureau of Transportation Services estimates that the average light-duty vehicle in the US emits 157 mg of NOx per mile driven. Such a car would thus be subject to a one-off registration tax of $1,989 in Norway.

The CO2 tax is assessed similarly to the NOx tax except that it is a progressive tax with rates that increase along with how much carbon a vehicle emits per mile driven. The following graph sums up the CO2 tax schedule.

According to the Department of Energy, the average light-duty vehicle produced in 2021 emitted 348 grams of CO2 per mile driven. Such a vehicle would have faced a $27,167 tax in Norway.

Like the CO2 tax, the vehicle weight tax is assessed progressively, with heavier vehicles being taxed at a higher rate than lighter vehicles. Prior to 2023, electric vehicles were not subject to the weight tax. In 2023, they will be subject to a weight tax but at a much lower rate than non-electric vehicles. The following graph sums up the weight tax schedule.

Taken together, the vehicle taxation regime reflects a clear policy agenda aimed at heavily discouraging the use of non-electric personal vehicles, especially big ones. And it works. In 2011, only 1 percent of new vehicles in Norway were zero-emissions vehicles. In 2022, the number is up to 78 percent.

So while the taxes above seem quite steep, they can largely be avoided by buying an electric vehicle, especially a light one. And that's what the vast majority of Norwegians now do.

2. The Wealth Tax

In the 2023 tax proposal, Norway has a progressive wealth tax with two rates: 1 percent of valued wealth between $166,600 and $1.96 million and 1.1 percent of valued wealth exceeding $1.96 million.

This is not a simple net worth tax because not all wealth is valued at its market price.

For the purposes of the wealth tax, primary homes are valued at 25 percent of their market price between $0 and $980,000 and 50 percent of their market price beyond $980,000. Second homes are valued at 95 percent of their market price.

Shares of stock and investment real estate are valued at 80 percent of their market price while non-dwelling fixed assets are valued at 70 percent of their market price.

These partial valuations shield a lot more wealth from the wealth tax than the nominal wealth tax brackets would suggest.

They also tend to make the wealth tax more progressive as primary homes make up a much smaller share of the portfolios of the very wealthy than they do the rest of the population.

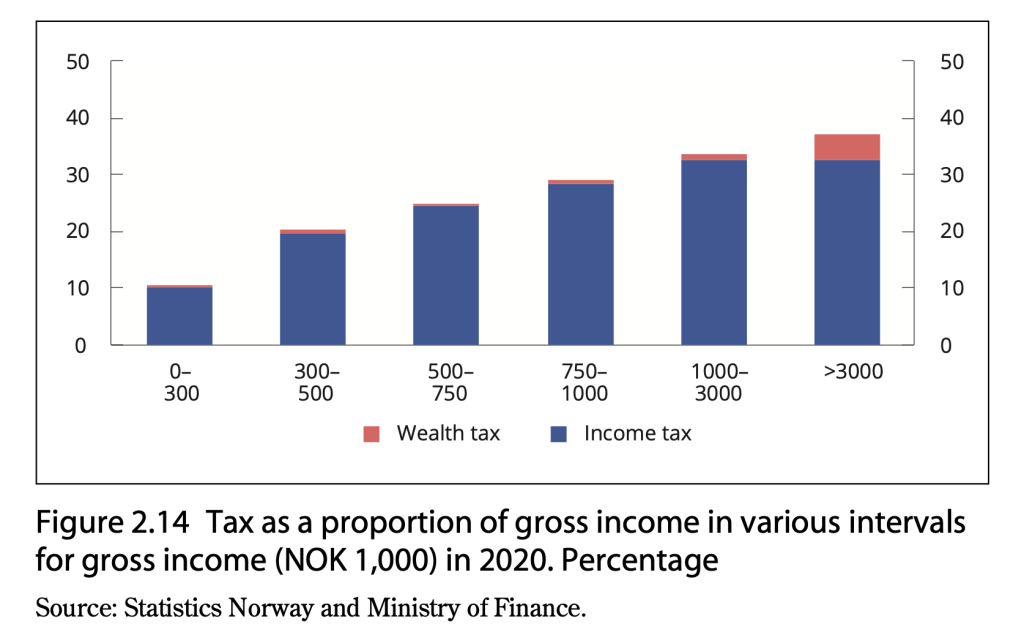

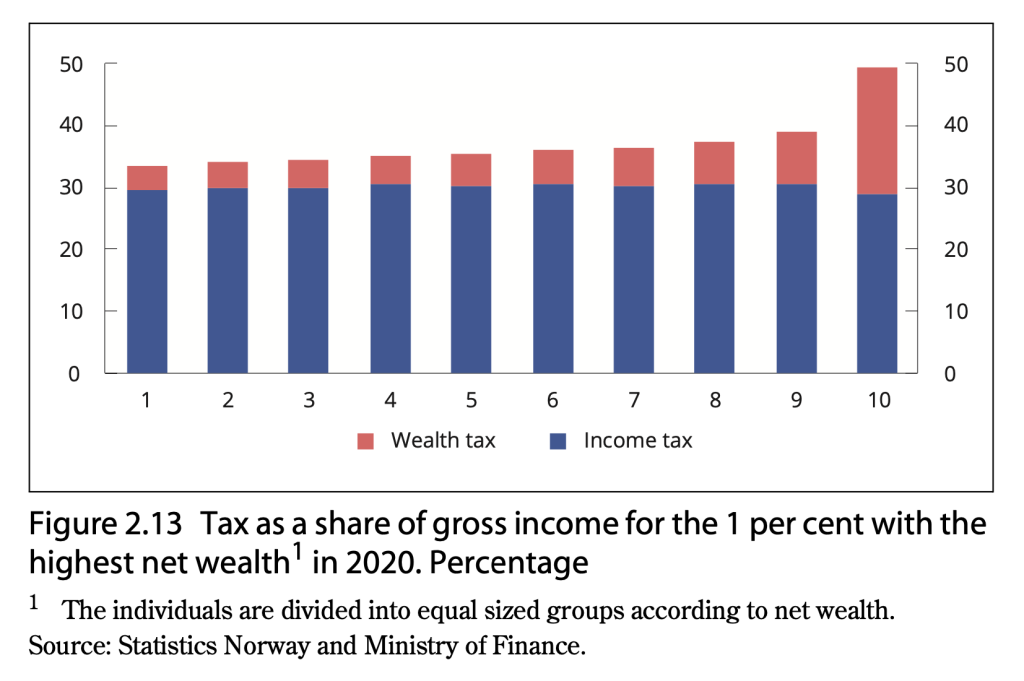

As one would expect, the wealth tax is highly concentrated on the richest and wealthiest people in Norway.

In fact, the Norwegian wealth tax is the only reason that the overall progressivity of Norway's tax system holds up at the very top of the Norwegian wealth and income distributions.

3. Overall Progressivity

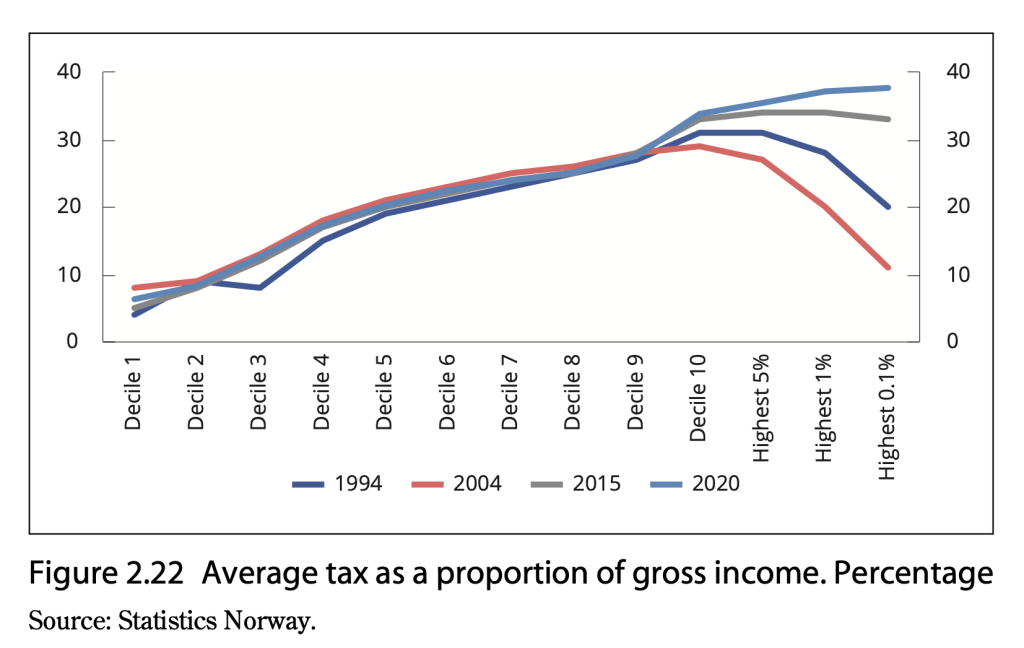

There is a common line in US discourse about the Nordic countries that says that they do not have progressive tax systems. I've written many times about the basic meaninglessness of this point, but it's also worth pointing out that, though this may have been true in the late 1990s and early 2000s after a conservative wave of governance had run through the region, it's not really true now, at least not in Norway.

The claim that Norway had regressive taxes was based primarily on three observations: 1) its taxes on labor — the general income tax, bracket tax, and payroll tax — are only slightly progressive, 2) it uses a dual income tax system that taxes capital income less than labor income, which ends up lowering the taxes of the upper class, 3) it has high consumption taxes, which hit the lower and middle class more (as a percent of income) than the upper class. Since the progressivity of (1) is surely overwhelmed by the regressivity of (2) and (3), it seems like it must be that Norway has an overall flat or regressive tax system.

But according to number-keepers in Norway, this has not been the case since around 2006 when dividend taxes were sharply increased in the country (the 2023 proposal increases them another 2 percentage points). Nowadays, the country's capital income taxation and wealth taxation ensure that the distribution of direct taxation is progressive all the way up the ladder.

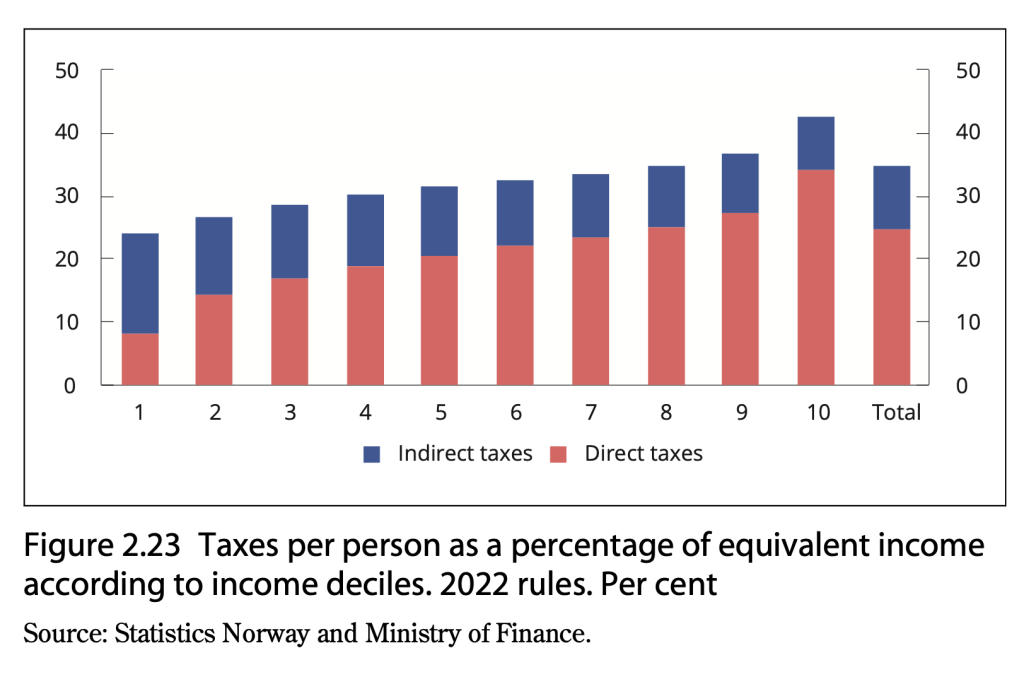

Adding the indirect taxes, which includes the dreaded regressive consumption taxes, does not negate this overall progressivity.

As noted already above, the idea that tax progressivity is an important goal in and of itself is, in my view, quite mistaken. But nonetheless, with appropriate levels of wealth and capital income taxation, it is possible to ensure an overall progressive tax scheme even with the kind of heavy consumption taxes that the US currently lacks.

4. Tax the Resource Rents

Norway is nothing if not invested in the idea that the proceeds of natural resource wealth should be captured collectively rather than by private owners. Thus, as of 2022, it had a special 71.8 percent corporate tax on oil companies on top of extensive state ownership in the oil sector. It also had a special 47.4 percent tax on hydropower rents, a sector where there is also extensive state ownership. In the 2023 tax proposal, the hydropower tax is being increased by 10.3 percentage points to 57.7 percent.

Building on this base, the government is now proposing a special resource rent tax on the aquaculture sector, which uses the ocean to farm salmon and other fish primarily for export, and the onshore wind energy sector. From the proposal:

The government made it clear in the Hurdal Platform that local communities and society as a whole should receive a fair share of the value created from the utilisation of society’s natural resources. The principle that society as a whole should receive a share of the profits generated from the utilisation of society’s natural resources has served Norway well. Without this, we would not now have the Government Pension Fund. Like the petroleum and hydropower resources, aquaculture and wind power resources are tax objects that cannot be relocated, and which should be taken advantage of at a time when many tax bases are becoming more mobile. The government is now proposing the introduction of a resource rent tax on aquaculture and onshore wind power, which will enter into force from the 2023 income year.

Much of the tax discourse focuses on things like how much the rich pay versus how much the poor pay or how the tax code can be used to incentivize or disincentivize certain behaviors. But scouring the economy for natural resource rents — which are produced by nature, not by any person — and fashioning the tax code to capture this free money for the common good is something all governments should try to do.

5. Tax the Rich to Combat Inflation

The tax proposal contains one last item worth noting, mostly for the way it is presented than its particulars. Currently, Norway has an employer-side payroll tax, similar to Social Security and Medicare taxes here. It is a flat tax assessed on all earnings, though the rate varies by region as part of a general policy goal of leveling out geographical disparities in income.

For 2023, the government is proposing to increase this tax by 5 percentage points for earnings beyond 750,000 NOK (~$73,500). It justifies this proposal, which is quite a significant break from the flat-tax tradition for employer-side payroll taxes, this way:

The government is seriously addressing the challenges ordinary people face in their everyday lives, such as the rapidly increasing prices on a variety of necessities. ... As a measure appropriate for the situation, the government proposes additional employer’s National Insurance contributions throughout the entire country for salaries in excess of NOK 750,000 in 2023. This measure will contribute to increasing the room to manoeuvre in the budget by about NOK 6.4 billion and enables stronger redistribution. The overheating labour market and the surplus of vacancies indicate that it is a good time to introduce additional employer’s National Insurance contributions

The US discussion on inflation control has variously shifted between arguments about whether inflation was meaningfully happening, whether it is happening due to a handful of dysfunctional sectors, and whether using interest rate hikes to try to tamp down inflation would do more harm than good.

Despite there previously seeming to be a lot of interest on the left in the idea of using taxes and spending to control the price level, virtually nobody has so far proposed to do so in the face of the current inflation.

Norway's move is thus notable because the left-wing government is at least giving lip service to the idea of increasing taxes on higher-earners — in this case indirectly through an assessment on their employers, which those employers may actually struggle to pass through in the short run — as an economy-cooling measure. Such a thing is of course unthinkable in the US, not least because of President Biden's commitment to not raise taxes on anyone earning less than $400,000. But, on the merits, it seems like such a thing should be in the mix, especially if we think that the income-distributive and capital-allocation effects of rate hikes are far worse.