In the United States, unemployment benefits are financed by employer-side payroll taxes and then administered by state agencies. The benefit amounts are earnings-related, meaning that they are designed to replace a percentage of an individual's prior earnings up to a point. There is technically a minimum unemployment benefit level that eligible recipients cannot fall below, but it is very low, and eligibility for this benefit does not extend to all unemployed people, only unemployed people with a sufficient work history.

Overall, the US unemployment system is quite bad, both in its design and in its practical functioning. This naturally raises the question of whether other countries do it better and, if so, whether we should copy them.

One alternative approach to unemployment benefits is called the Ghent System. Broadly speaking, in this system, unemployment benefits are managed by unions and financed by union member dues. This system originated in Ghent, Belgium, but has taken its most prominent form in the Nordic countries.

Although the Ghent System is broadly understood as union-run unemployment benefits, the actual operation of unemployment insurance (UI) in Ghent countries is more complicated than that. In the three Nordic countries that have some version of the Ghent System — Finland, Sweden, and Denmark — the state is still heavily involved in unemployment benefits in three main ways:

- State transfers, not union dues or unemployment insurance premiums, finance the vast majority of the union-administered unemployment benefits.

- The state directly provides a basic unemployment allowance — either through a specific unemployment benefit or through a more general social assistance benefit — for unemployed individuals who are not eligible for the union-administered unemployment benefits.

- The state, through regulation, mostly dictates the parameters of the unemployment benefits provided by the unemployment funds.

These aspects of actually-existing Ghent Systems are important for understanding how they work. They also provide an insight into some of the flaws of the system, which are the same flaws that pop up every time a country tries to organize a welfare benefit through a voluntary private insurance scheme.

When the Ghent System began in the late 19th century, unions attempted to run them as purely voluntary schemes that were fully financed with member dues. This led to an adverse selection problem where individuals that were less likely to experience unemployment abstained from membership to avoid paying UI premiums. This also led to risk-pooling problems because each union's membership was concentrated in one sector and so, if an economic shock hit that sector specifically, the union's unemployment fund would quickly run out of money. These two issues frequently left union unemployment funds insolvent and therefore unable to actually provide members with insurance against unemployment.

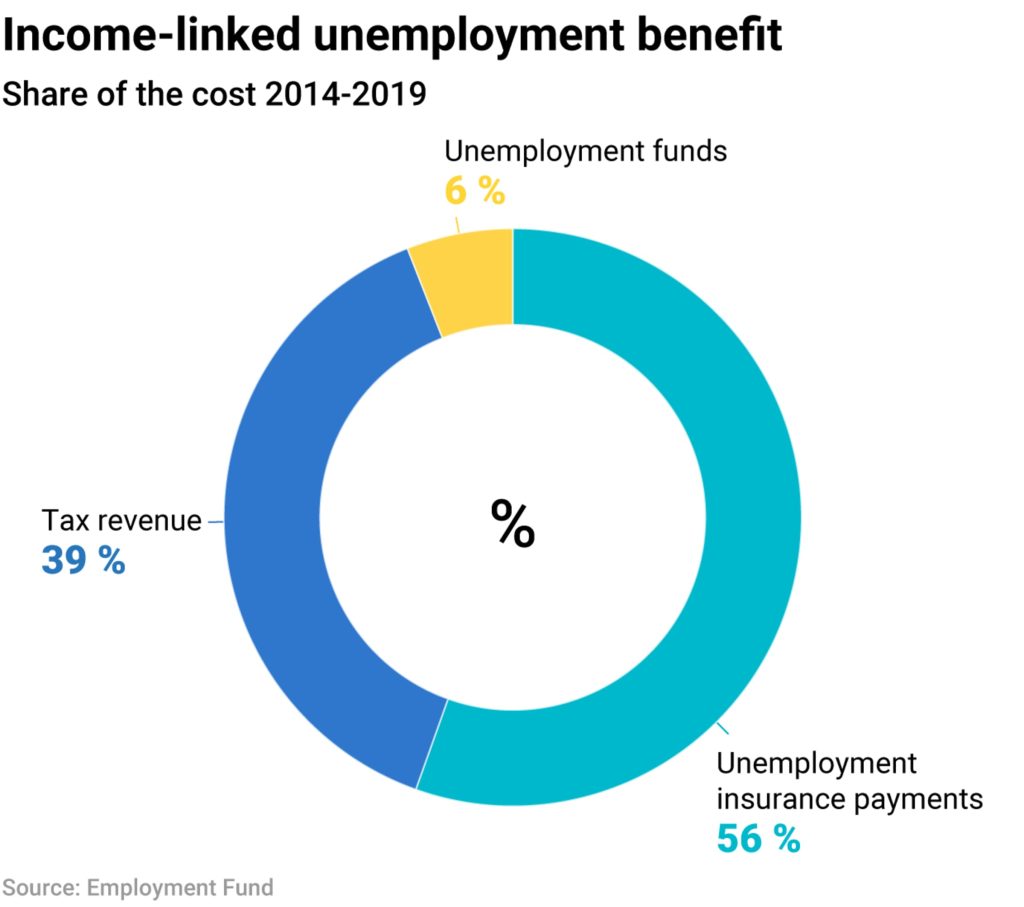

In order to fix this problem, the state had to step in and begin funding the benefits through public appropriations. In the below graph, we can see what this looks like in contemporary Finland where the government finances 94 percent of the union-administered UI program (unemployment insurance payments are what we call payroll taxes). The voluntary member UI premiums only cover the remaining 6 percent of the cost.

Government funding in this way resolves the adverse selection problem by making contributions effectively compulsory and by bringing the out-of-pocket premiums down so low that abstaining from fund membership because you have a low risk of unemployment does not make any financial sense. The funding also diversifies risk across the entire economy because the taxation is applied economy-wide instead of in each sector.

Government funding is able to fix the solvency problems of the initial regimes, but it is not able to fully fix the non-participation problems of them. The government subsidies make it so that it is very financially unwise to not participate in an unemployment fund, but insofar as people still have to actively sign up well in advance of becoming unemployed to participate, the scheme has administrative burdens that result in some non-participation.

For example, in Finland, around 15 percent of the workforce is not enrolled in one of the unemployment funds. These workers are disproportionately young and concentrated in lower-paying jobs. Some of these workers may be making a financial calculation that even the tiny out-of-pocket premiums are not worth the insurance, but others probably just lack a familiarity with the system and do not understand how or why they should sign up.

In Sweden, around 30 percent of the workforce is not enrolled in one of the unemployment funds.

In order to fix this problem, the governments directly administer a basic unemployment benefit to people not eligible for benefits from an unemployment fund. This benefit is sometimes administered explicitly as an unemployment benefit. Other times, it is administered as a general "social assistance" benefit. But in each case, the benefit is not tied to prior earnings and is offered as a flat amount. This resolves the problem of large minorities of the workforce not participating in an unemployment fund, but it does not provide the same kind of protection as those funds do. These workers effectively make contributions to unemployment funds through taxes but don't receive benefits from them because they failed to enroll.

Funding most of the cost of the unemployment funds while also catching the workers that fall through the cracks of the system still leaves a potential problem when it comes to the specific parameters of the benefits offered by the funds. The benefit rules cannot be left totally up to the funds themselves both because those rules matter for macroeconomic management but also because the government needs to make sure that its financing of the benefits actually achieves the goal of providing the desired level of protection against unemployment.

So the government has to step in and set most of the unemployment benefit rules for the various funds. The funds do differ some in what they charge and how much they pay but, by and large, they are very similar because of the state regulations.

Overall, this scheme actually looks a bit like the Obamacare health insurance exchange scheme we have in the US. In that scheme, people enroll in a health insurance plan with the financing for that plan mostly coming from government subsidies and with the rules for that plan being mostly dictated by the government. The subsidies are necessary to get people to sign up and the rules are necessary to ensure the plans actually provide the desired level of protection against ill health.

But even with all of this, a large chunk of people eligible to sign up for a subsidized exchange plan simply do not do so, including many people who are eligible for a premium-free exchange plan. Unlike with the non-participants in the unemployment funds discussed above, our government has no backup plan for these non-participants and they simply go uninsured.

Given these flaws, you may be wondering why the Nordic countries, which are generally known for their relatively pristine welfare designs, run their unemployment benefits this way?

In answering this question, it's worth noting initially that not all of them do. Norway does not use the Ghent System and instead runs both the earnings-related and basic allowance components of their unemployment scheme through the centralized welfare institution. Unions play no role.

For the others, the reason is that it is widely believed, and there is very good evidence to suggest, that the unemployment funds system increases union membership. This is not because you actually have to be a member of a union to sign up for a fund. The precise situation differs across the countries, but generally speaking, there are unemployment fund options that are not run by unions or run by fake unions and you can sign up for unemployment benefits without also paying member dues. But the norm is to sign up as a union member alongside enrolling in an unemployment fund, and so it still nudges more people into membership than the alternative.

This is beneficial to unions from a financial perspective because they can get more dues-paying members than they would otherwise get. And certainly better financing probably makes them more effective as unions. But union power is ultimately rooted in the genuine willingness of workers to participate in strike actions not how many paper members they have. Norway's union membership numbers are lower than the surrounding Nordics that have a Ghent System, but they are still quite high internationally speaking and their ability to pull off union actions, which again is not strictly related to the size of their paper membership, seems fairly similar.

Overall, then, I do not find the Ghent System to be all that tempting. Insofar as union strength is absolutely essential to the creation of an egalitarian society, I can understand why the Nordic countries that use the Ghent System may decide that more robust unions are worth the cost of a non-ideal unemployment benefits system. And of course, their unemployment system is still far better than what the US has. But I'd rather have a fully centralized unemployment system like Norway has than the Ghent Systems of its Nordic neighbors.