Last week, Jeanna Smialek wrote a piece at the New York Times that was partially a Stephanie Kelton profile and partially a commentary on Modern Monetary Theory (MMT) in light of the pandemic. More than anything else, the piece is just really confusing and strange. It starts from the premise that MMT got "tried out" during the pandemic, but this premise is just very clearly wrong.

Countercyclical Policy Is Normal

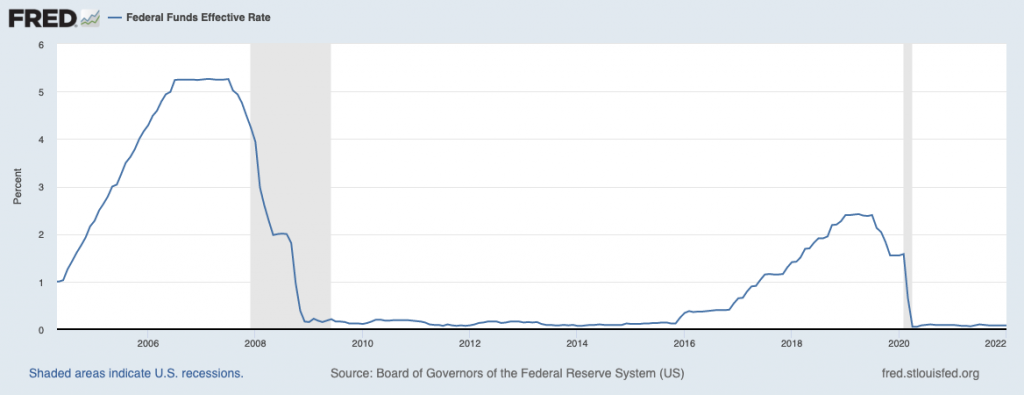

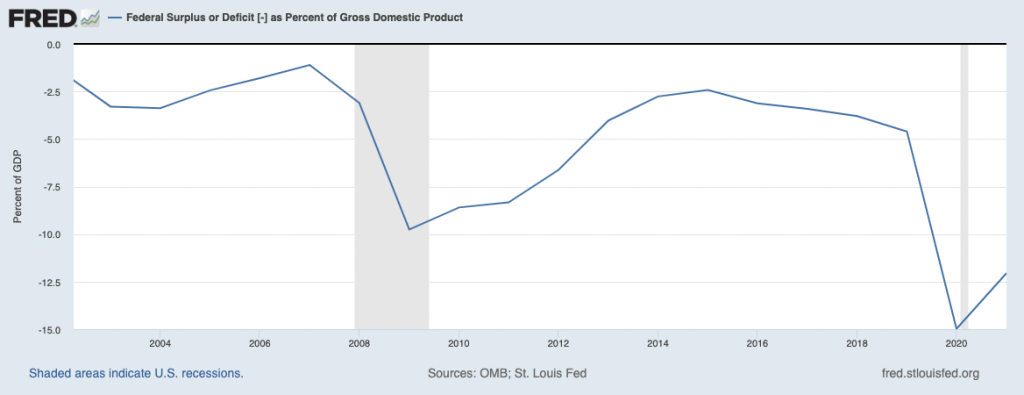

Our response to the coronavirus recession has not been that much different from our response to the Great Recession in 2008.

In both cases, the Federal Reserve cut interest rates to zero.

In both cases, the federal government pursued deficit-financed stimulus.

Even the shape of the stimulus packages were similar. Both packages included extended unemployment benefits, expansions to the child tax credit and the earned income tax credit, aid to state and local governments via grants to school districts and increases in federal support for Medicaid, and "stimulus checks" of one sort or another.

The fiscal response was bigger this time around, but so too was the severity of the recession.

If our response to the coronavirus recession was an "MMT tryout," then was our response to the Great Recession also an "MMT tryout"? Is "doing MMT" just doing fiscal and monetary stimulus to help pull the country out of a recession? Is it when you increase the government deficit by 10.3 percent of GDP (coronavirus recession) instead of increasing it by 8.6 percent of GDP (Great Recession)? Are those 1.7 points where the MMT kicks in?

MMT Policies Were Not Tried

Another way you could claim that we did an MMT tryout would be to point out some of the MMT-favored policy items we implemented. MMT advocates do not just say we should have countercyclical fiscal and monetary policy — something almost every economist says — but also have some specific approaches to countercyclical policy.

One thing they tend to push for is overt monetary financing of fiscal deficits. So rather than selling bonds to finance deficits and then separately having the Federal Reserve, at its discretion, create money to buy those bonds, many MMT people are really big on just directly spending the created money. Indeed, some MMT advocates actually got Rashida Tlaib to include this "coin seignorage" in one of her stimulus bills. But it didn't pass. No overt monetary financing ever happened.

Another thing they tend to push for is the "job guarantee" approach to managing unemployment. Prior to the pandemic, MMT advocates spent a lot of their time arguing that we should manage unemployment by having unemployed people do community service for the minimum wage. As part of this advocacy, they also spent a lot of their time slamming the idea of cash welfare benefits, which they said were dangerously inflationary. When the pandemic hit, the most hardcore JG advocates in the MMT ranks — Pavlina Tcherneva and Randy Wray — said we needed to do a JG right away. Wray even went as far as saying we should do the JG instead of "ramping up jobless benefits." As with overt monetary financing, the coronavirus recession response did not feature a JG and was instead handled almost entirely with the kinds of cash benefits that MMT advocates have tended to criticize.

The latter point has been one of the most interesting developments in the MMT world over the last year. After spending years defining themselves against broad-based cash transfers and putting up a slight fight against them at the beginning of the pandemic, the MMT advocates seem to have come around entirely on them in the last 1.5 years or so. Either for political-coalitional reasons or a desire to claim credit for ongoing policy, or perhaps both, the MMT world has basically stopped talking about job guarantees while supporting helicopter drop after helicopter drop.

Inflation and MMT

When reading Smialek's piece, one question you have to ask yourself is: what would have to happen to discredit MMT? What economic indicator would need to go in which direction after what series of actions in order to show that the MMT advocates are wrong?

Smialek makes no effort to answer that question even though her piece is ostensibly focused on the success or failure of MMT, both its theory and advocates. For many MMT critics, the answer to the question is that you should look at whether inflation ran up after a stimulus bill. If it did, then a lot of what MMT says in its public advocacy is basically discredited.

The reason for thinking this is that MMT advocates regularly say things that imply we could have a full blown social democratic welfare state without raising the tax level at all. Indeed, it is these proclamations that actually seem to be the secret of its appeal to certain progressives.

Hitting 7 percent inflation well before we even sniff a social democratic welfare state would thus seem to throw cold water on all of this. The MMT shortcut we were promised doesn't actually exist.

Conclusion

With this all said, I think it is important to distinguish the article that Smialek wrote from an evaluation of Kelton per se. Kelton has certainly said some odd things about the pandemic response. The idea that (1) conventional monetary and fiscal stimulus, (2) that no MMT advocate had any direct role in, (3) that focused on cash benefits, (4) that lacked overt monetary financing and a job guarantee, and (5) that was followed by high inflation is a major feather in the cap for MMT is a bit comical. But it's also not really Kelton's fault that Smialek did a bad job with the profile. Smialek's failures are not Kelton's failures and it would be unfair to conflate them.