In 2008, Washington State enacted a cash benefit program called the Working Families Tax Credit (WA WFTC) but failed to provide funding for it for fifteen years. The program recently became funded for the first time and is expected to begin providing benefits to people this year.

The WFTC has been widely celebrated by progressive organizations in Washington and touted as a major economic justice win for low-income Washingtonians. But as I demonstrate in the analysis below, it is actually a very badly designed program that will exclude around half of low-income children from benefits.

Program Design

The Washington Working Families Tax Credit (statute, regulations) is based on the federal Earned Income Tax Credit (EITC). Under the rules of the WA WFTC program, Washington families that file a federal tax return and that are eligible for the federal EITC can claim up to $1,200 of benefits from the WA WFTC by separately filing an application to the Washington Department of Revenue with their federal tax return attached to that application.

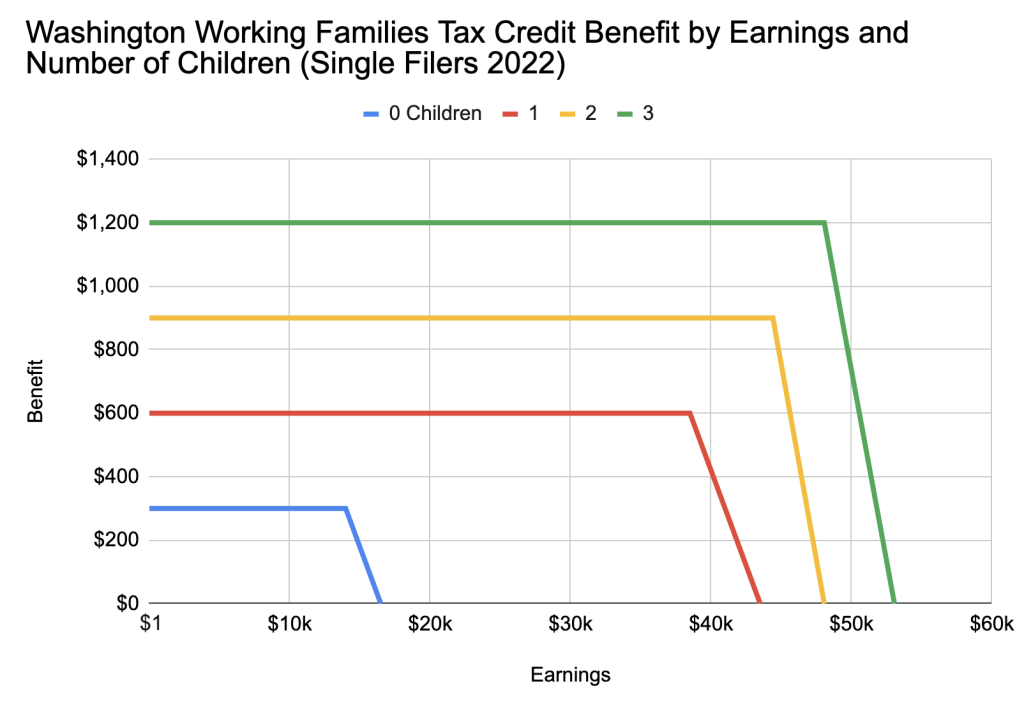

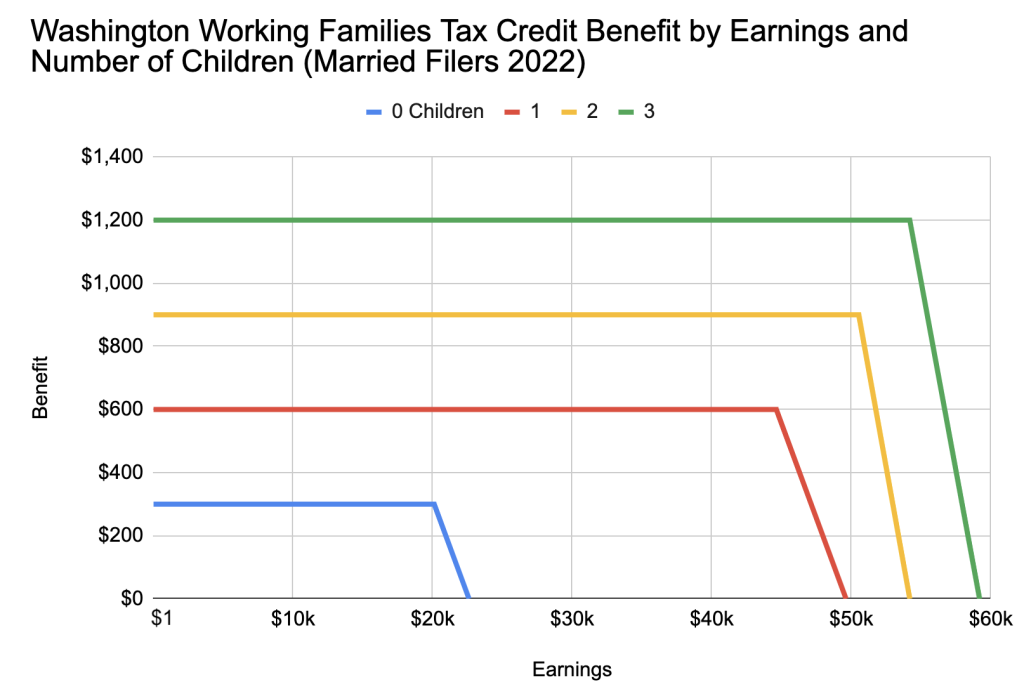

The precise amount of the WA WFTC benefit varies by each family's tax-filing status, income, and number of children. The following two graphs neatly summarize these program parameters.

Like the federal EITC, the WA WFTC includes a tiny benefit for some childless adults between the ages of 25 and 64 (the blue line above), but it is primarily a benefit for children. For this reason, I will focus most of my analysis of the program on families with children.

Half of Low-Income Kids Will Be Excluded

On first glance, the WA WFTC program appears to be designed to ensure that all Washingtonian children living in lower income families receive a few hundred dollars each year. But this will not happen for three reasons:

- Children living in families with $0 of earnings are not eligible for the WA WFTC benefits.

- Children living in families that do not file federal income tax returns are not eligible for WA WFTC benefits.

- Children living in families that fail to separately apply for the WA WFTC will not receive WA WFTC benefits.

Using Census and IRS data, we can estimate what percent of Washingtonian kids will be excluded by reasons (1) and (2). We do not know yet how many will be excluded by reason (3), but it is likely to be substantial.

According to the Annual Social and Economic Supplement of the Current Population Survey (CPS ASEC), there were around 1,786,000 children in Washington in 2021. Around 117,000 (6.5 percent) of those children lived in tax units that had no earnings and were therefore ineligible for the federal EITC. The percentage of children living in tax units without earnings varies by race, as we can see in the graph below.

These children are too poor to receive the EITC and, because WA WFTC eligibility is based on EITC eligibility, also too poor to receive the WA WFTC.

The above graph uses the entire child population for its denominator. But the WA WFTC is meant to be a benefit for low-income children. So in this next graph, I show what percent of low-income Washingtonian kids live in tax units without earnings. For these purposes, a kid is considered low-income if their family income is not too high to be ineligible for the EITC.

Overall more than one in four low-income Washingtonian kids live in families that had no earnings in 2021. For low-income black kids, the number is nearly one in two.

Around 73.4 percent of low-income kids in Washington are eligible for the federal EITC. If all of them filed a federal tax return and subsequently filed a WA WFTC application, then that is how many would receive WA WFTC benefits. But that level of participation is not going to materialize.

According to the IRS, 25.6 percent of Washingtonian families that are eligible for the federal EITC do not apply for it, typically because they do not file federal tax returns. This indicates that, in addition to the 26.6 percent of low-income kids who are too poor to receive the WA WFTC, another 18.8 percent of low-income kids will be ineligible for the program because their family does not file federal income taxes. Combined, these two exclusions will keep 45.4 percent of low-income kids out of the WA WFTC program.

For the 54.6 percent of low-income kids whose parents have nonzero earnings and file federal taxes, there is one last obstacle to claiming WA WFTC benefits, which is that these parents will have to file a separate benefit application with the WA Department of Revenue with their federal tax return attached.

Unlike other state tax credit programs, this is not something that they will do as part of filing their state income taxes because Washington has no state income tax. So this will truly have to be a standalone application only for this benefit that is not part of any other administrative process.

It's hard to say for sure how many people will fail to jump through this hoop, but if the participation rates of other welfare programs are any indicator, the number will be substantial. If we assume very conservatively that only 10 percent of people will fail this hurdle, then that knocks another 5.5 percent of low-income kids out of the WA WFTC program, bringing the combined total to one in two low-income kids.

Enact a Universal Child Benefit for Washington

Unlike Washington's paid family leave program, the WA WFTC cannot be easily fixed with a few tweaks. The entire administrative framework underlying it is an unworkable mess that is incompatible with high participation rates among the target population. It is what happens when someone is tasked with creating a state version of the already bad federal EITC in a state that does not even have a state income tax that the tax credit can be added to.

The whole appeal of these credits is supposed to be that it is easy to sign up for them because you just check a box on the tax forms you already have to file. The downside to this is that it does not actually work when you are dealing with low-income populations because many low-income families do not file taxes. But in Washington, the downside to the tax credit approach goes beyond that because literally nobody files state income taxes because they do not exist.

There are presently eight states in the country that lack a state income tax. One of those states, Alaska, pays out an annual cash benefit to its residents called the Alaska Permanent Fund Dividend. Given Washington's similar administrative constraints, the Alaska PFD program is clearly a better model for a Washington child benefit program than state-level EITC programs in states that have income taxes.

A Washington Child Benefit program loosely modeled on the Alaska PFD would only really need two fiscal parameters:

- A dollar amount paid annually to every single child resident of the state.

- A payroll tax that raises enough revenue to pay for (1).

Washington has no state income tax, but it currently has three payroll taxes: one that funds Worker's Compensation, another that funds Unemployment Insurance, and a third that funds Paid Family and Medical Leave. As an administrative matter, it would be trivial to add a fourth payroll tax to fund the Washington Child Benefit.

According to the CPS ASEC, Washingtonians earned around $285 billion in 2021. The Quarterly Census of Employment and Wages (QCEW) similarly reports total annual wages in Washington at $277 billion. A one percent payroll tax applied to the QCEW base would generate $2.77 billion of revenue, enough to provide $1,548 to all 1,785,000 children in the state. A 0.5 percent payroll tax would be enough to provide a universal child benefit of $774.

A Washington Child Benefit so designed would require an application process, but that process would be much simpler than the WA WFTC process. It would not require applicants to prove their income nor would it require them to file federal taxes. All that would be necessary is for them to certify their residency in the state. As with the Alaska PFD, after an individual has signed up once, subsequent years of benefits could be as simple as re-certifying on a website that your residency status and information is unchanged from the year before.

When people propose universal benefits like this, one common objection is that they waste too much money providing benefits to the affluent. But this is a mistaken understanding of how these benefits work. The amount someone would (net) benefit from the scheme described above is equal to the amount they receive from the child benefit minus the amount they pay in the payroll tax. The lowest income people will pay no payroll tax and thus receive the most (net) benefit. As you move up the earnings scale, the child benefit amount stays the same, but the payroll tax amount rises, driving the (net) benefit down. Thus, such a scheme actually provides (net) benefits that are directly proportional to income, with the bottom receiving the most, and the top receiving the least (indeed the top actually pays more in tax than they receive in child benefits).

In general, this kind of "universal" design is superior to the typical "means-tested" design that tries to use each person's income to determine what their benefit payment should be. But this is especially true in the case of Washington where the lack of a state income tax means that it simply does not have the administrative ability to cleanly execute a means-tested tax credit.

This is the second piece in our series on Washington State. This series is being done in collaboration with the Washington Community Alliance.