Cory Booker released some details of his new American Opportunity Account Act proposal on Monday (Vox, Senate). Under the proposal, the federal government would use 18 years to capitalize a social wealth fund and then, in year 19 of the program, start using the fund to pay out means-tested grants to 18-year-olds. The grant recipients would only be able to use the money for approved purposes such as education fees, a down payment on a house, or contributions to a retirement account.

The Fund

The centerpiece of Booker's proposal is the capitalization of a moderately-sized social wealth fund. To understand how this would work, it is useful to put some hard numbers to it.

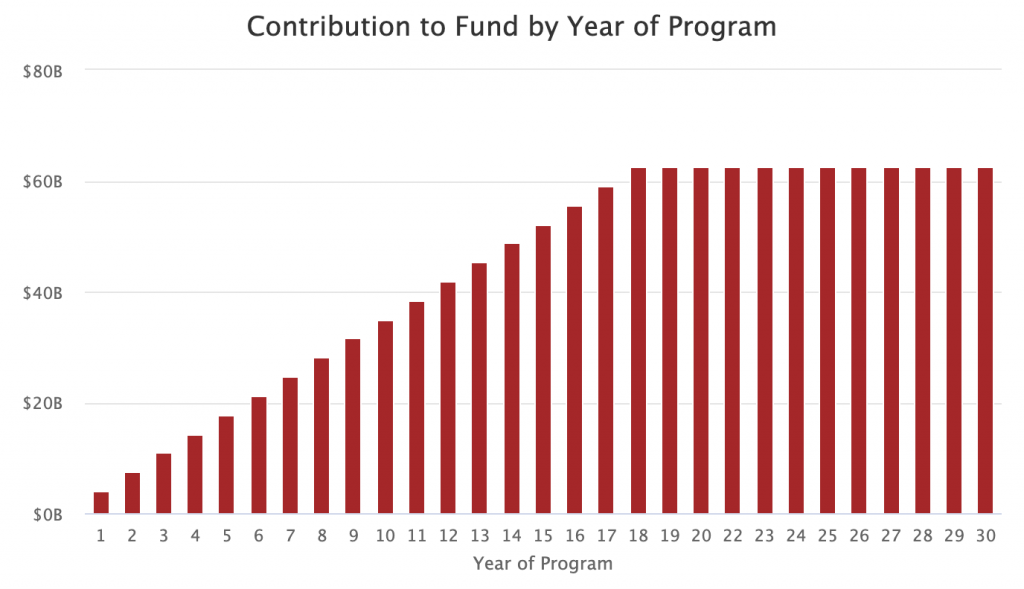

According to the plan, $1,000 is deposited to the fund every time a child is born. From there, according to Vox's reporting on the plan, an average of $861 is deposited every year for every child between the ages of 1 and 17. These supplementary deposits phase in initially such that in year 2 of the program the $861 is only deposited for every 1-year-old, in year 3 the $861 is only deposited for every 1-year-old and 2-year-old, and so on.

If you assume that around 4 million children are born each year, then the annual contribution into the fund starts at $4 billion in year one of the program. It then steadily rises based on the phase-in method discussed above so that $62.5 billion is contributed in year 18 of the program and every year after that.

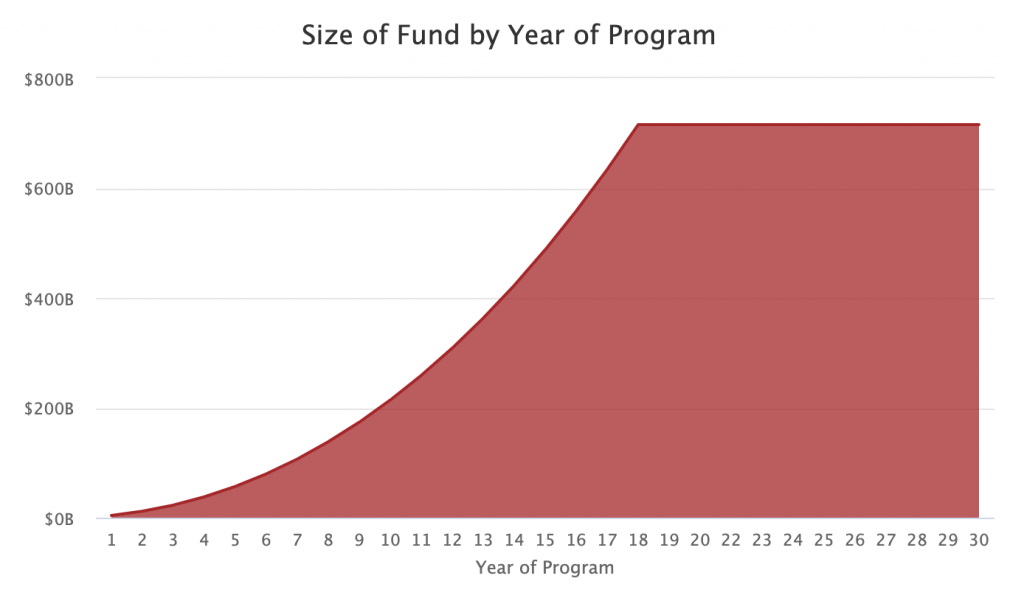

Booker says he intends to invest the fund's capital conservatively with the goal of achieving a 3 percent nominal rate of return. Based on the contribution schedule above and the same assumption of 4 million annual births, the fund will grow in size to around $715 billion in year 18 of the program. The fund's size levels out in year 18 because, in year 19 and every year afterwards, the program pays out lump sum grants to 18-year-olds.

After the fund is fully capitalized in year 18, it will be putting off around $19 billion per year in investment returns. That return is then combined with the $62.5 billion annual contribution to finance the annual grant for 18-year-olds. To be clear, this is not how Booker frames what he is doing, but this is the cleanest explanation of how it would work overall.

The Grant

Starting in year 19 of the program, every 18-year-old would receive a grant of money. According to Vox's piece on the proposal, the average grant would be around $21,000. The precise grant given to each individual varies based on the earnings record of their parents during the prior 18 years. Thus, 18-year-olds whose parents had high incomes during their childhood will receive a lower grant while 18-year-olds who parents had low incomes during their childhood will receive a higher grant.

Grant recipients will not just get a $21,000 check, but instead will be forced to put the money towards a list of approved items. Right now, the three items mentioned are education fees, down payments on a home, and retirement accounts. The goal here is to ensure that the money goes into building each individual's wealth in some way.

Good Things

From my perspective, the main good thing about the program is that it is at least an entry point into the idea of a dividend-paying social wealth fund, something we have been pushing here at People's Policy Project. The core feature of Booker's plan is to build up a moderately-sized pile of publicly-owned capital, the return from which will be paid out in the form of a grant to 18-year-olds. This is structurally similar to my social wealth fund proposal, just much more modest in scope.

Bad Things

The bad things about the proposal are unfortunately somewhat numerous.

-

- The program provides no tangible benefit for 18 years. This will make the program easy to kill before it ever reaches its crucial inflection point in year 19. This is what happened when the same program was tried in the UK. Tony Blair created accounts like this in 2004, but they were killed six years later under David Cameron before ever delivering benefits to anyone.

-

- The program only provides benefits to 18-year-olds. If the program manages to survive until year 19, it still faces the problem that it only provides one-off benefits to 18-year-olds. This means the only people who stand to benefit from the program's preservation are those who are too young to vote. This is true in a sense of all child-focused programs, but most of those programs also provide indirect benefits to parents as well. A grant only for 18-year-olds has such a narrow constituency that it may fail to be politically resilient.

-

- It uses severe means-testing. According to the Vox coverage, 18-year-olds would receive grants ranging from $1,681 to $46,215 based on the earnings records of their parents. This kind of means-testing, like all means-testing, is going to degrade public support for the program. It is also going to prove difficult to implement because it requires a clean income record for each 18-year-old's parents. Squaring that need with the fact that very poor families often don't file income tax returns and that children often juggle between tax units and households will not be easy.

- It restricts how the grants can be spent. As with the means-testing, the spending restrictions are going to create administrative difficulties because the government has to keep up with what people are doing with the money. The restrictions will also invariably end up forcing some people to put the money towards things that are not as useful to them as what they want to put it towards. Finally, the restrictions may end up being futile as well. What's to stop someone from buying a house and then selling it immediately in order to get the cash clear and free of government restrictions?

The Alternative

The best alternative to Booker's social wealth fund proposal is, of course, my own social wealth fund proposal. That proposal provides annual dividends to all adults starting in year one and continues to grow the size of the underlying fund into perpetuity.

But if one insists on doing a program that involves providing lump sum grants to 18-year-olds, there are ways of doing that better as well.

First, eliminate the means-testing and provide all 18-year-olds the same grant. This will make the program more popular and get rid of administrative headaches. To the extent that the means-testing exists to make the program more redistributive overall, that can be achieved on the tax side of things.

Second, start providing the grants to 18-year-olds right away. The ostensible reason why Booker's plan waits nearly two decades before actually providing grants to anyone is because it uses that time to capitalize the (in the exercise above) $715 billion social wealth fund. But you do not need 18 years to capitalize a social wealth fund that large. At the end of last month, the total market capitalization of publicly-traded US companies was around $32 trillion. This means that a one-off 2.2 percent market capitalization tax, payable in scrip rather than cash, could capitalize the fund in year one. This should allow you to start paying out grants in year two.

Finally, get rid of the restrictions on what the money can be spent on. This keeps the administrative costs and surveillance of the program down. It also allows people to put the money towards the best use as they see it. If you do not trust that 18-year-olds can spend lump sum grants wisely, then you probably should reconsider the whole premise of the program in the first place.