On Wednesday, I wrote a piece responding to a truly bizarre ProPublica article that conflated money corporations borrow from the bond markets with free cash given out by the government to households and small businesses. There have been some responses and further efforts to make sense of this completely bewildering piece that I will address below.

More ProPublica Screw Ups

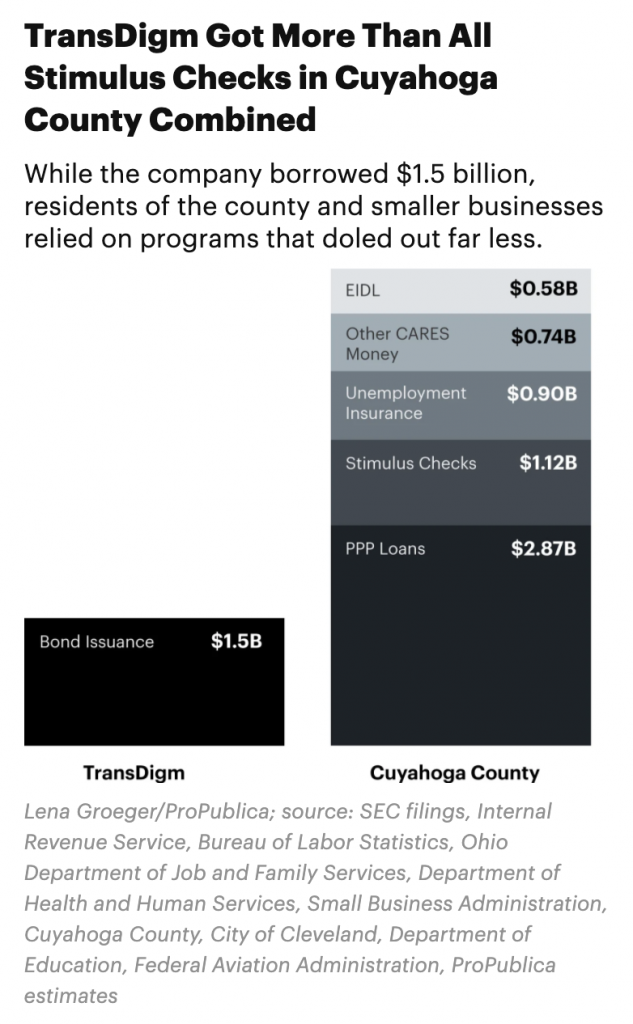

Before I get into responses though, let me add another funny wrinkle into this story that the crack team at ProPublica somehow missed. To understand this wrinkle, it is necessary to recall that at the center of the ProPublica piece is this strange graphic where they compare bonds issued by TransDigm with free money given out to residents and small businesses in Cuyahoga County.

Putting aside the silliness of pretending like borrowed money is the same as cash grants, the more sophisticated message here is supposed to be something like: the Federal Reserve cutting interest rates is why TransDigm borrowed $1.5 billion from the bond market, which is bad. But when you look into TransDigm, it becomes clear pretty quickly that even the factual premise of this statement is wrong.

TransDigm borrowed $1.5 billion with private issues in April of this year (I, II). This was before the Fed's Secondary Market Corporate Credit Facility (SMCCF) became operational. Worse than that, TransDigm's bonds are not investment grade and have not been investment grade for many years. This means that the company's debt is not even eligible to be purchased by the SMCCF or other Fed operations.

Even if you put aside the fact that these are ineligible junk bonds issued before the Fed's corporate credit facilities began, in order to believe that the Fed's activity caused this particular issuance, you'd want to at least establish that it was an atypical issuance for the company. But looking back just one year reveals the company issuing $4.55 billion of junk bonds on terms that are actually better than the terms they got for their $1.5 billion issue in April of 2020 (the April 8 issue has a whopping 8% interest rate). So the chosen poster child of Fed-induced borrowing actually did less than one-third of the borrowing in 2020 than they did in the ordinary times of 2019.

Misdirected Grievances

The bewildering choice of TransDigm whose operations don't even fit the story makes more sense once you understand that the whole motivation for the piece really has nothing to do with the Federal Reserve interest rate policy. David Dayen makes this clear in his response piece where he argues that the $1.5 billion of cash TransDigm raised is bad because TransDigm is a bad company that does bad things with their money. Put simply: Dayen has longstanding grievances with TransDigm and has decided to shoehorn those longstanding grievances into an argument about whether the interest rate on corporate debt should be lowered in a recession.

I sympathize of course with being mad at bad companies. But I have no idea what that has to do with setting interest rates on debt or economic stimulus more generally. Should you push interest rates up so long as some people and businesses who borrow money are bad actors? Should the PPP loans have included scrutiny of every business that applied to see whether they were a good business that did good things rather than a bad business that does bad things? Obviously not. This would be an absurd and impossible thing to administer and weeding out bad actors is best handled by law enforcement not the terms of credit or eligibility for grants.

To be fair to Dayen, he does at one point in his piece seem to make the much more general claim that actually all or most big corporations are bad actors that do bad things with money they borrow. That seems a bit over the top, but even supposing it's true, it seems like his objection is not with the Fed's corporate credit facilities but rather with corporate credit period. That's fine I suppose as far as things go, but again just seems weirdly shoehorned in here. Corporations borrowed money when the interest rate was 0.25pp higher too (over $1.5 trillion in new bonds were issued last year). And in some sense the Fed was to blame for that as well seeing as it has the power to completely blow up corporate credit markets and the financial system more generally but chooses not to, including in 2019 when the Federal Reserve did the unthinkable and maintained an interest rate policy that allowed TransDigm to borrow $4.55 billion.

Scattershooting

In addition to misdirected grievances, proponents of the ProPublica-endorsed argument have been engaging in various scattershooting efforts where they hamfistedly try to surface new and disconnected claims to be able to finally prove that lowering the pre-COVID interest rate by 0.25pp is a world-historical injustice.

The first such effort I saw came from who else but David Dayen. In his newsletter, Dayen got suckered by the Americans for Financial Reform into claiming that the Federal Reserve is actually overpaying for the bonds they have purchased in the SMCCF (as an aside, nobody ever seems to mention how many bonds the Fed has actually purchased; it's only $12.4 billion). Dayen's evidence for this claim is as follows:

Americans for Financial Reform ferreted this out in a criminally under-discussed revelation. The Fed reports its corporate bond purchases and loans under the CARES Act to Congress; the most recent one came out September 8. If you go to the trade-level data for bond purchases, you see this very clearly. There’s a par value, a market rate for the bond purchases the Fed is making. It’s paying more than par with virtually every purchase. It bought Altria (the Marlboro and Juul people) bonds at 109.9 percent. It bought Columbia Pipeline group at 116.7 percent. It bought Principal Financial Group at 112 percent. All but a very few of hundreds of purchases totaling tens of billions of dollars are made above par. On average, the price is 107 percent.

Dayen wrongly believes that corporate debt trades at its face value, as if traders just keep selling the same bond over and over again at the same price. In reality, the market price of bonds fluctuates along with the interest rate environment. The par value is not the market value. Paying more than the par value in a secondary purchase is not paying more than the market value. Dayen simply does not know what he is talking about and unfortunately, like the ProPublica writers, allowed himself to be bamboozled by a motivated organization.

The second effort came from Matt Stoller. Stoller links to an article about non-public corporations borrowing $15 billion in September and using $4 billion of it for dividends. Stoller believes this is a great slam dunk that proves lowering the corporate bond rate by 0.25pp is a massive giveaway to corporations. But this confuses the corporate bond market for the bank loan market. The Fed is buying in the former not the latter.

Worse than that though, the $15 billion does not even seem to be high. The same story says that $55 billion of these loans were issued in October 2016, the record month. It does not say anything about any other months, but $15 billion seems to be pretty normal, and is also small potatoes in the corporate debt world. For comparison, according to Bloomberg, new corporate bond issues totaled $257 billion last month. This puny market is less than 6 percent of that.

Conclusion

As I noted in my initial post on Wednesday, probably the best word for all this misdirected angst and scattershooting in which the theory of the problem changes every few weeks is "undertheorized."

What is the correct interest rate here? 1%? 2%? 3%? 4%? The exact rate that obtained the day before the pandemic hit? Is the problem with lower rates that they make debt that would have been borrowed anyways cost less or is the problem that they induce companies to take on more debt? How is the Federal Reserve responsible for the $1.5 billion of junk bonds TransDigm borrowed in April 2020 but not for the $4.55 billion of junk bonds they borrowed in February of 2019? How is the Federal Reserve responsible for the $15 billion of corporate bank loans in September 2020 but not the $55 billion they borrowed in October 2016 or the regular amount they just borrow every month?

And if the Fed is responsible for all of it at all times because all finance depends on the central bank, then what does that have to do with CARES or recent rate cuts? Does this also logically mean that for instance the SEC is responsible for it (you can't issue securities without its approval)?

It genuinely is hard to figure out what on earth the argument is here and of course it does not help that it seems to shift every day. If you want a more comprehensible take on things, I'd strongly recommend this piece published in Salon in September of 2015, which argued that higher interest rates would slow the economy, slow wage growth, lock-in high unemployment for black people, and exacerbate income inequality. The author? David Dayen.